Real estate investing works best when it is treated as a system, not a one-time property purchase. Beginners need to understand how financing, appraisal, buying, negotiating, managing, and selling connect before they risk money on an investment property.

The easiest mistake in real estate investing is to focus only on the property. A house looks cheap, a rental seems promising, or a seller appears flexible, so the beginner jumps straight to the deal.

I would slow that down. A property is only one part of the investment. The financing changes the return. The purchase price shapes the exit. The tenant process affects cash flow. The records determine whether the investment is being run like a business or guessed at month to month.

The practical answer is simple: successful real estate investing needs a repeatable process. Secure financing, identify value opportunities, analyze the property, negotiate carefully, manage the asset, keep records, and plan how you may eventually sell or reposition it.

Takeaways

- Start with financing because leverage, loan structure, and down payment requirements shape what kind of property you can safely pursue.

- A good buy is built around price, motivation, improvement potential, favorable financing, and keeping your initial cash investment controlled.

- Appraisal matters because a property must be judged by value, income potential, and comparable alternatives—not excitement alone.

- Property management is where paper profit becomes real performance through tenant screening, rent collection, maintenance, budgeting, and records.

- Selling should be planned before you need to sell, because timing, pricing, documents, buyer qualification, and negotiation room all affect the final result.

Understanding the Real Estate Investment Lifecycle

Real estate investing begins before the purchase and continues long after closing. A beginner should think in stages: financing, finding, analyzing, negotiating, managing, and exiting.

That sequence matters because each stage affects the next. Financing determines what you can buy. Appraisal helps you avoid overpaying. Negotiation shapes your starting position. Management protects income. Selling turns accumulated value into realized profit.

A simple investment lifecycle looks like this:

- Financing: Understand available loan structures, down payment needs, and funding sources.

- Property search: Look for opportunities such as motivated sellers, fixer-uppers, foreclosures, HUD-owned homes, or other bargain sources.

- Appraisal and analysis: Estimate value using practical valuation methods before making an offer.

- Negotiation and offer: Set terms for deposit, purchase price, balance due, closing date, and possible counteroffers.

- Management: Handle tenants, maintenance, rent collection, budgeting, and records.

- Exit strategy: Decide whether to rent, sell, use a lease-option, convert, refinance, or hold for longer-term income.

The real lesson is that a property is not “good” in isolation. A property bought at the wrong price, with the wrong financing, poor tenant controls, and weak records can become a burden. A modest property bought well and managed carefully can become a stronger investment than a more impressive property handled carelessly.

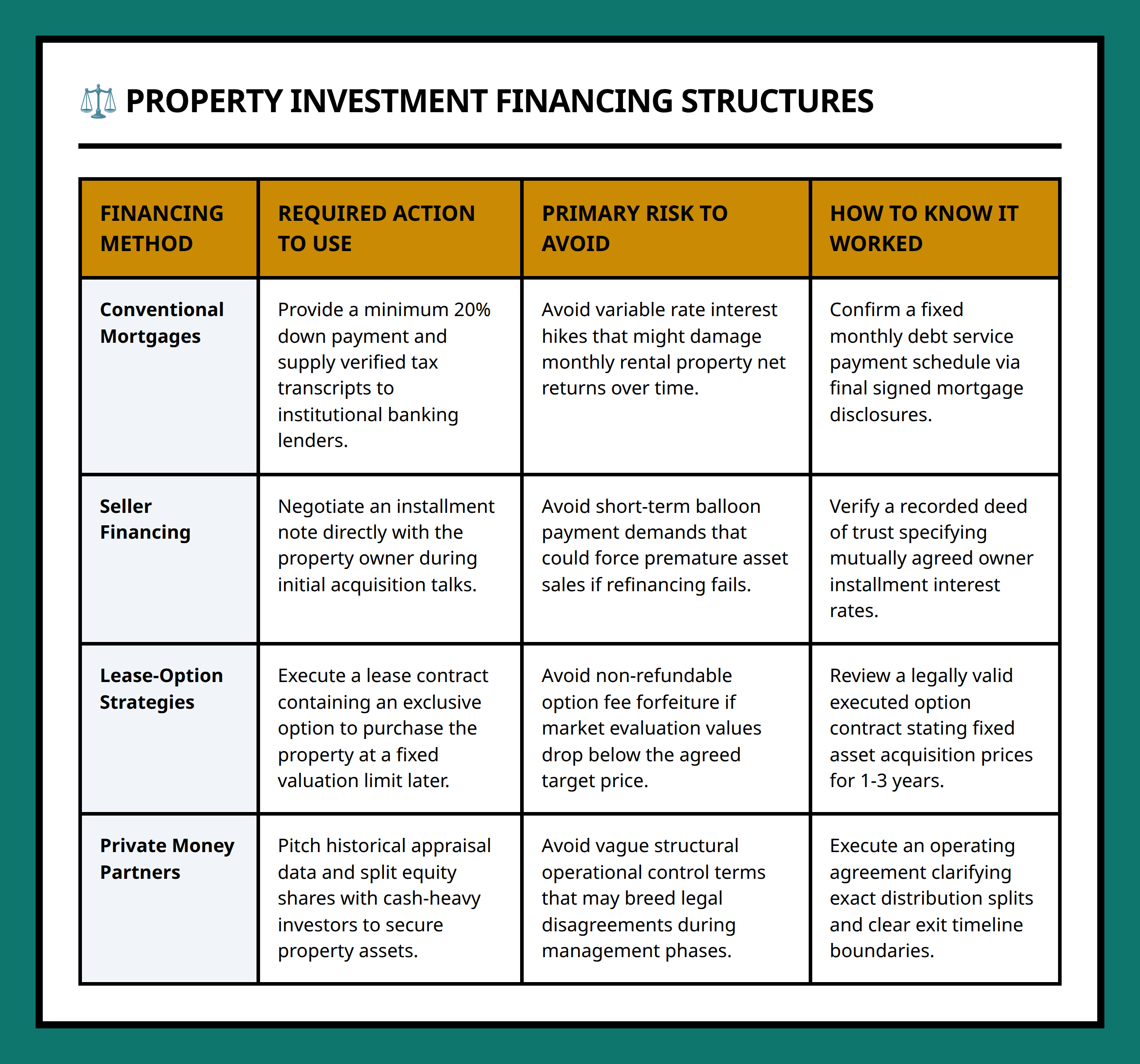

Financing Comes First Because It Controls the Shape of the Deal

Financing is the engine of real estate investing because it affects both purchasing power and risk. Leverage allows an investor to control property with borrowed money, but the structure of that debt changes the investment’s flexibility.

Beginner investors should become familiar with common loan ideas before shopping seriously. These include interest-only loans, fully amortized loans, partially amortized loans, adjustable-rate loans, graduated loans, loan underwriting, loan-to-value ratio, discount points, and loan assumption.

That may sound like a lot, but the practical question is plain: What will this financing require from me now, and what pressure will it create later?

For example, an illustrative beginner might compare two similar small rental properties. One requires more cash down but has simple payment terms. Another requires less cash up front but has a more complicated financing structure. The second deal may look better because it preserves cash, but it still has to be judged by payment stability, future flexibility, and whether the property can support the obligation.

Real estate financing can come from several sources. Existing property sellers may play a role. Savings and loan associations, commercial banks, credit unions, insurance companies, loan brokers, and partnerships can all appear in the funding picture. Some sources are more suited to short-term financing, some to permanent financing, and some to larger commercial projects.

The beginner’s job is not to memorize every financing path at once. The job is to avoid treating “Can I buy it?” as the only question. A better set of questions is:

- How much cash will I need at purchase?

- What kind of loan payments will the property need to support?

- Are there points, assumptions, impounds, or closing costs to understand?

- Will the financing make it easier or harder to sell later?

- Does this financing leave enough room for repairs, vacancy, and mistakes?

Finding Value Starts With Buying Right

The strongest real estate investments often begin with the purchase terms. If you overpay at the beginning, management has to work harder just to recover from the mistake.

A useful beginner rule is: buy right so you have room to sell right. The ingredients of a good buy include purchasing at a good price from motivated sellers, choosing fixer-uppers where sweat equity can be created, assuming low-interest loans when possible, and buying with as little down as practical.

A motivated seller is someone whose circumstances may make them more willing to consider a lower or more flexible offer. Examples include job relocation, a vacant rental, landlord fatigue, lack of money, a property that has been on the market for a long time, or another property already purchased.

That does not mean pressuring people. It means paying attention to the reason a seller may value speed, certainty, or simplicity. A seller with a vacant rental and ongoing headaches may care about a clean closing more than a seller who is just testing the market.

Fixer-uppers also deserve careful judgment. The most beginner-friendly opportunity is not always the property with the most dramatic repair needs. A property that mainly needs cleaning, paint, and manageable cosmetic work is very different from one with major structural or system problems. Sweat equity works best when the investor can reasonably understand the work, the cost, and the likely value improvement.

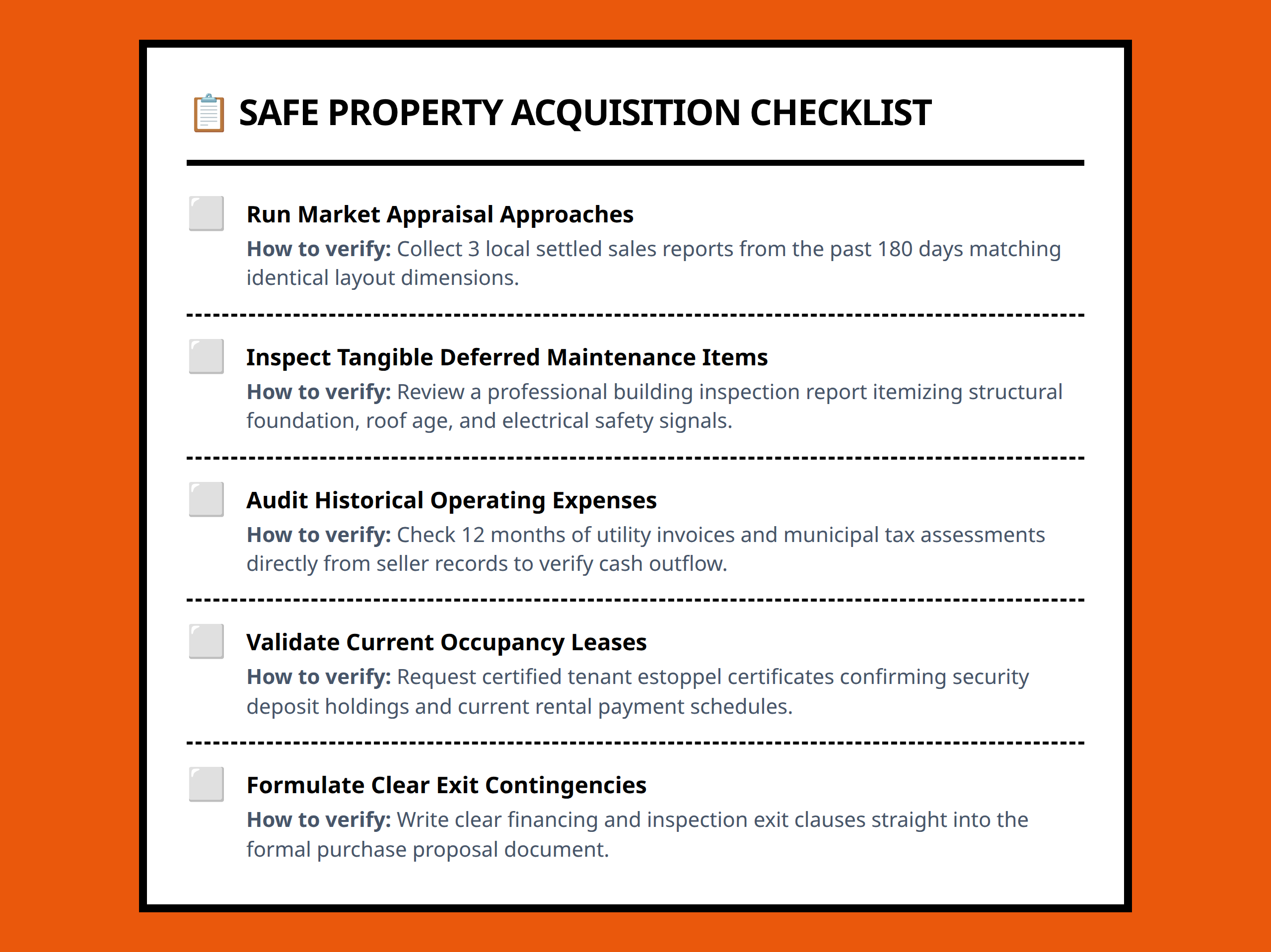

Use Appraisal Thinking Before You Make an Offer

Appraisal is the discipline that keeps enthusiasm from becoming overpayment. Before making an offer, a beginner should learn to ask, “What is this property worth, and why?”

Several appraisal approaches can help shape that answer:

| Appraisal approach | What it helps you judge |

|---|---|

| Market-data method | How the property compares with similar properties that have sold. |

| Reproduction-cost method | What it would cost to reproduce the structure, adjusted for relevant value factors. |

| Capitalization method | How income-producing property value relates to income. |

| Gross-income multiplier method | How gross income can be used as a simplified comparison tool for income property. |

For beginners, the exact method matters less than the habit behind it. Do not judge a property only by asking whether it feels affordable. Judge it by price, income, comparable value, condition, financing, and your exit plan.

Here is a simple way to apply appraisal thinking. Imagine a small rental that looks attractive because the monthly payment seems manageable. Before calling it a deal, compare it with similar properties, estimate needed repairs, look at likely rent, and think about whether the future sale price would leave enough room after costs. That is appraisal thinking in everyday language.

Negotiation Turns Analysis Into Terms

Negotiation is where your analysis becomes a written offer. The offer should not be vague. It should clarify the earnest-money deposit, the balance of the purchase price, the closing date, and other terms that matter to the deal.

Beginners often think negotiation is mainly about price. Price matters, but terms can matter too. A lower deposit, a workable closing date, favorable financing, or a carefully structured contingency can change the practical risk of the transaction.

Counteroffers are part of the process. A seller may reject one term while accepting another. The investor’s job is to know which terms are essential and which ones can move.

I like to think of an offer as a test of discipline. If the numbers only work when everything goes perfectly, the offer is probably too fragile. If the offer still gives room for repairs, vacancy, financing costs, and a realistic resale or rental plan, it is more likely to survive contact with real life.

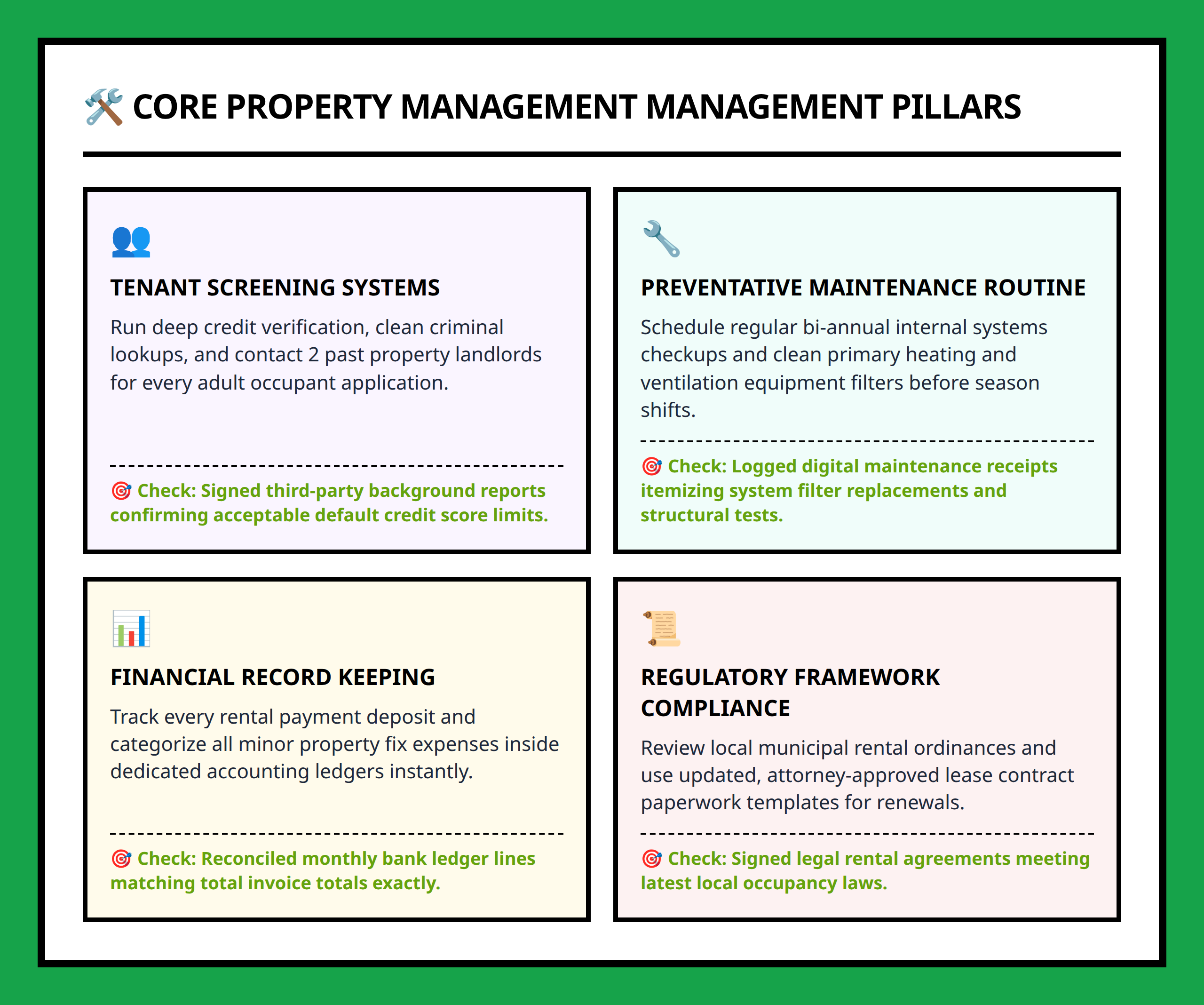

Property Management Is Where Returns Are Protected

Property management is not a side task. It is the operating system of a rental property. Poor management can weaken a good purchase, while careful management can preserve the value of an ordinary one.

The management work starts with practical choices: furnished or unfurnished units, appliances, utilities, trash removal, maintenance, repairs, interior painting, and preventive maintenance. These choices affect both the tenant experience and the owner’s costs.

Vacancy is another management issue. Showing and renting vacant units requires advertising, showing the unit, qualifying the prospective tenant, handling the move-in, and setting expectations for rent collection. A casual process here can lead to problems later.

A simple rental workflow might look like this:

- Prepare the unit with necessary cleaning, repairs, and paint.

- Advertise the vacancy clearly.

- Show the unit to prospective tenants.

- Use an application and check credit references when appropriate.

- Set rental terms in writing.

- Document the move-in condition.

- Collect rent consistently.

- Track income, expenses, repairs, and tenant issues.

For larger or more hands-on properties, a resident manager may be involved. That adds another layer: choosing the resident manager, setting rent-collection policy, supervising the manager, and keeping delinquency records when needed.

The point is not to make real estate sound complicated for its own sake. The point is that income property has moving parts. If rent collection, repairs, tenant qualification, and records are loose, the investment becomes harder to judge and harder to improve.

Records Turn a Property Into a Business

Good records help an investor see what is actually happening. Without records, a rental can feel profitable while quietly leaking money through repairs, vacancy, poor rent collection, or unmanaged expenses.

Useful records include a tenant card system, an income and expense journal, depreciation records, and an annual income statement. These are not just administrative details. They help the investor answer basic business questions:

- How much income did the property actually produce?

- Which expenses are recurring?

- Are repairs becoming a pattern?

- Is rent collection consistent?

- Is the property ready to support another investment decision?

This is where beginners should be especially honest. If you would not trust a business with no records, do not trust a property with no records either. Real estate may involve land and buildings, but the investment still needs numbers, documents, and follow-through.

Profit Can Come From More Than One Exit

A real estate investor should think about the exit before the exit is urgent. Selling is one route, but it is not the only way a property may create value.

Rental income is one path. Lease-option arrangements are another strategy, where renting and a future purchase option are connected. When using a lease-option, the important discipline is to put everything in writing and structure the option agreement clearly.

Other value paths may include selling the investment outright, converting the property to a different use when appropriate, or holding property for lifetime income. Each path requires different planning, and not every property fits every strategy.

If selling becomes the plan, preparation matters. The selling process involves timing the sale, pricing it right, gathering necessary documents, preparing the exterior and interior, using a property information sheet, advertising, holding an open house or using a “for sale” sign, handling the sales agreement, and qualifying the buyer.

Traditional residential selling guidance also warns that timing can affect buyer attention. Spring and fall are described as stronger selling seasons, while winter holiday periods may be weaker because buyers are often distracted. That seasonal idea should be used as a planning reminder, not as a substitute for current local market judgment.

Pricing deserves special care. A seller needs to know the least acceptable price, then allow some room for negotiation. Asking too much can reduce serious buyer interest. Asking too little can leave money on the table. The right price is not an emotional number; it is a strategy.

Common Beginner Mistakes to Avoid

Most beginner mistakes come from treating one part of the investment as if it stands alone. A good-looking property can still be a weak investment if the financing, price, repairs, records, or exit plan are wrong.

- Shopping before understanding financing: This can lead to chasing properties that do not fit your actual buying power.

- Ignoring appraisal discipline: A property should be compared, valued, and analyzed before an offer is made.

- Confusing cheap with valuable: A low price is not enough if repair costs, weak rent, or poor resale potential erase the advantage.

- Managing tenants casually: Weak screening, unclear terms, and inconsistent rent collection can damage returns.

- Skipping records: Without income, expense, depreciation, and annual records, the investor cannot clearly judge performance.

- Selling without preparation: Pricing, documents, buyer qualification, and negotiation room should be prepared before the property hits the market.

The better habit is to make each stage support the next one. Financing should support acquisition. Acquisition should support management. Management should support income. Records should support decisions. Exit planning should support profit.

FAQ

- Real estate investing: Buying, holding, improving, renting, financing, or selling property with the goal of producing income or profit.

- Leverage: The use of borrowed money to control a larger property investment than cash alone would allow.

- Loan-to-value ratio: A comparison between the loan amount and the value of the property. It helps lenders and investors judge financing risk.

- Appraisal: A process for estimating property value using methods such as comparable sales, cost, or income-based analysis.

- Market-data method: An appraisal method that looks at similar properties to help estimate value.

- Capitalization method: An appraisal method used with income property to connect property value with the income it can produce.

- Motivated seller: A seller who may be more willing to accept flexible or below-market terms because of personal, financial, vacancy, relocation, or property-related pressure.

- Sweat equity: Value created through work, repairs, cleaning, painting, or improvements rather than through cash investment alone.

- Lease-option: An arrangement that combines renting with an option to purchase the property under written terms.

- REO: Real Estate Owned property, often referring to property owned by a lender after foreclosure-related processes.

- MLS: Multiple Listing Service, a listing system that helps brokers and agents share property availability with a wider buyer market.

- Closing: The final stage of a real estate sale when documents are completed, money is settled, and the transaction is finished.

The simplest next step is to build a one-page investment checklist before looking at another property: financing, value, seller motivation, repair needs, offer terms, management plan, records, and exit. If one box is blank, the deal is not ready yet.