Algorithmic trading is primarily an execution tool, not a prediction tool. Its main purpose is to help market participants execute orders efficiently by reducing market impact, controlling execution risk, preserving anonymity, and improving access to liquidity.

When people hear the phrase “algorithmic trading,” they often imagine computers constantly searching for profits. While some trading systems do attempt to forecast prices, many algorithms exist for a much simpler reason: executing trades more effectively.

I think this distinction is one of the most overlooked parts of modern markets. Many institutions are less concerned with predicting the next price move than they are with completing large transactions without disrupting the market itself.

Takeaways

- Large orders can move market prices and increase trading costs.

- Algorithmic trading often focuses on execution quality rather than prediction.

- Breaking large orders into smaller pieces can reduce market impact.

- Hidden liquidity and iceberg orders help preserve trading anonymity.

- Algorithmic systems require monitoring because operational and market risks still exist.

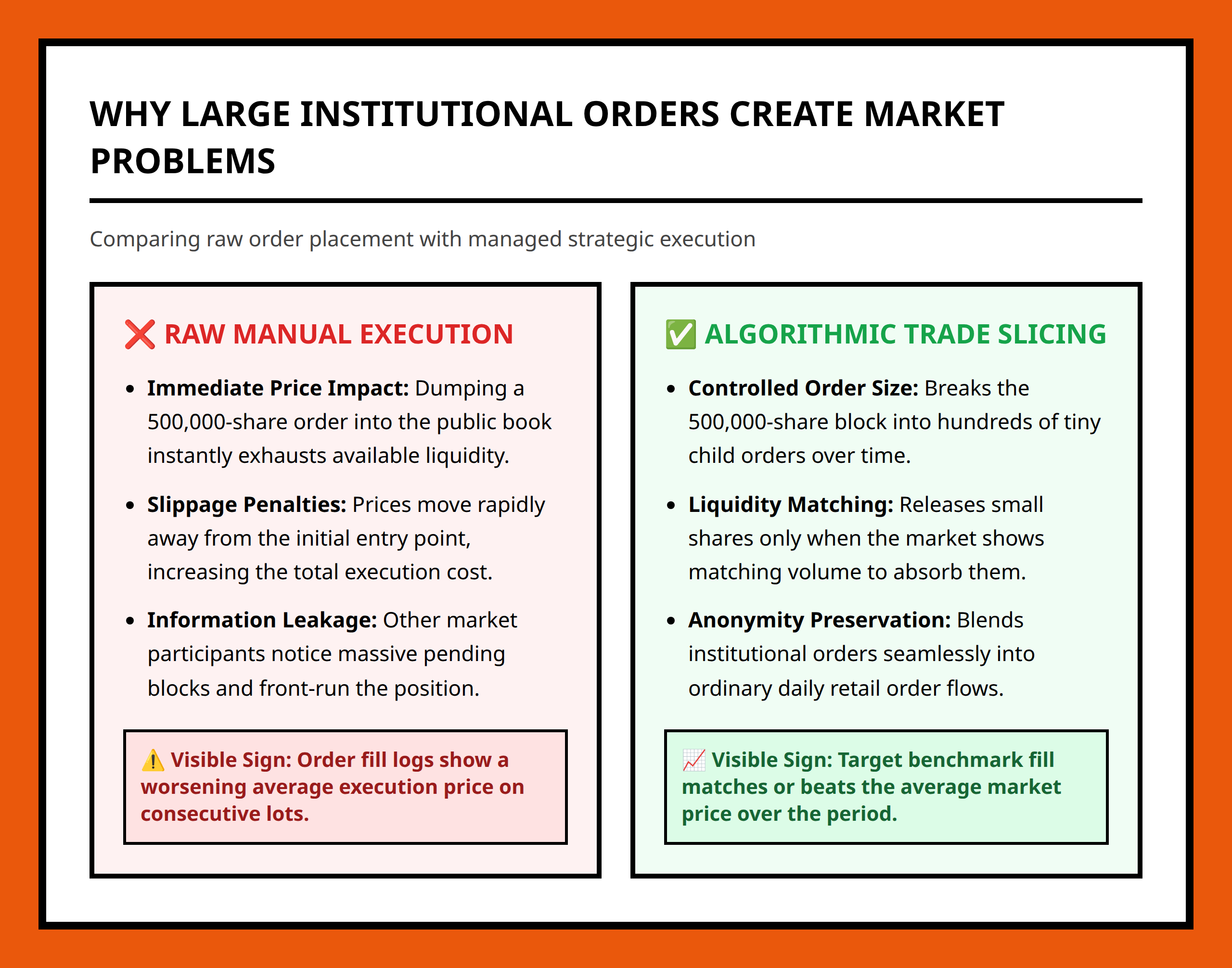

Why Large Orders Create Problems

Large trades can influence prices before the transaction is fully completed.

When a market participant attempts to buy or sell a significant quantity of securities, other participants may react to that activity. The resulting price movement can make the remaining portions of the order more expensive to execute.

This challenge is often called market impact. The larger the order relative to available liquidity, the greater the risk that prices will move before execution is complete.

Consider an illustrative scenario. An institution decides to acquire a large position. If the entire order is sent to the market immediately, other participants may recognize the demand and raise prices. The institution could end up paying more than expected simply because its own activity influenced the market.

Algorithmic trading emerged largely as a solution to this problem.

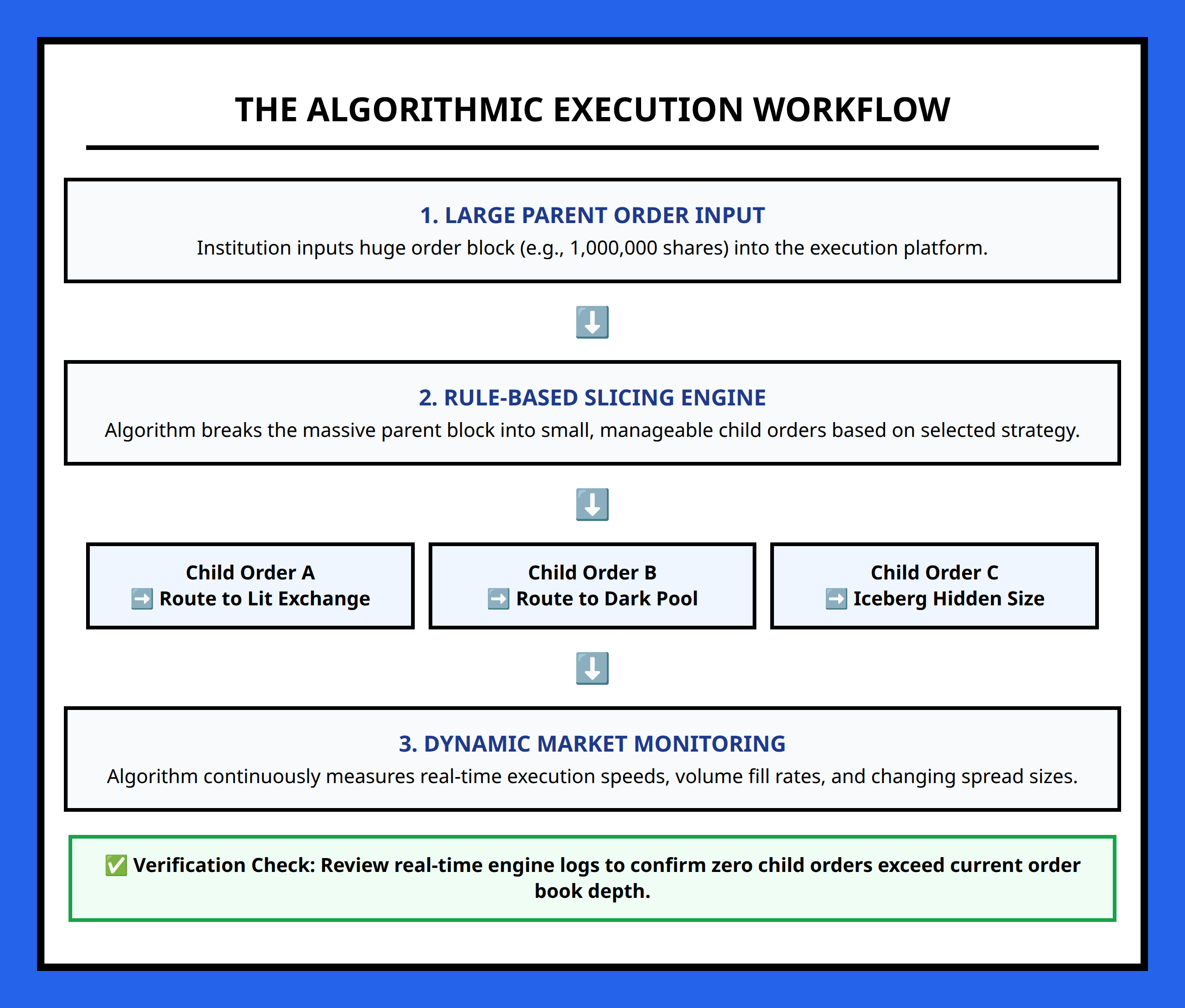

How Algorithmic Trading Works

Most execution algorithms work by dividing a large order into smaller transactions and distributing them across time, markets, or liquidity sources.

Instead of exposing the entire order at once, the algorithm follows predefined instructions that determine how and when portions of the order should be executed.

This process helps reduce visibility and may lower market impact. It also allows traders to seek better execution opportunities as market conditions change.

| Execution Step | Purpose |

|---|---|

| Order Analysis | Evaluate size, liquidity, and objectives |

| Order Slicing | Break large orders into smaller pieces |

| Routing | Send orders across available markets |

| Execution Monitoring | Track progress and adjust as needed |

| Completion | Finish execution while managing risk and cost |

The key idea is that the algorithm follows rules designed to improve execution quality rather than relying solely on human judgment during every stage of the trade.

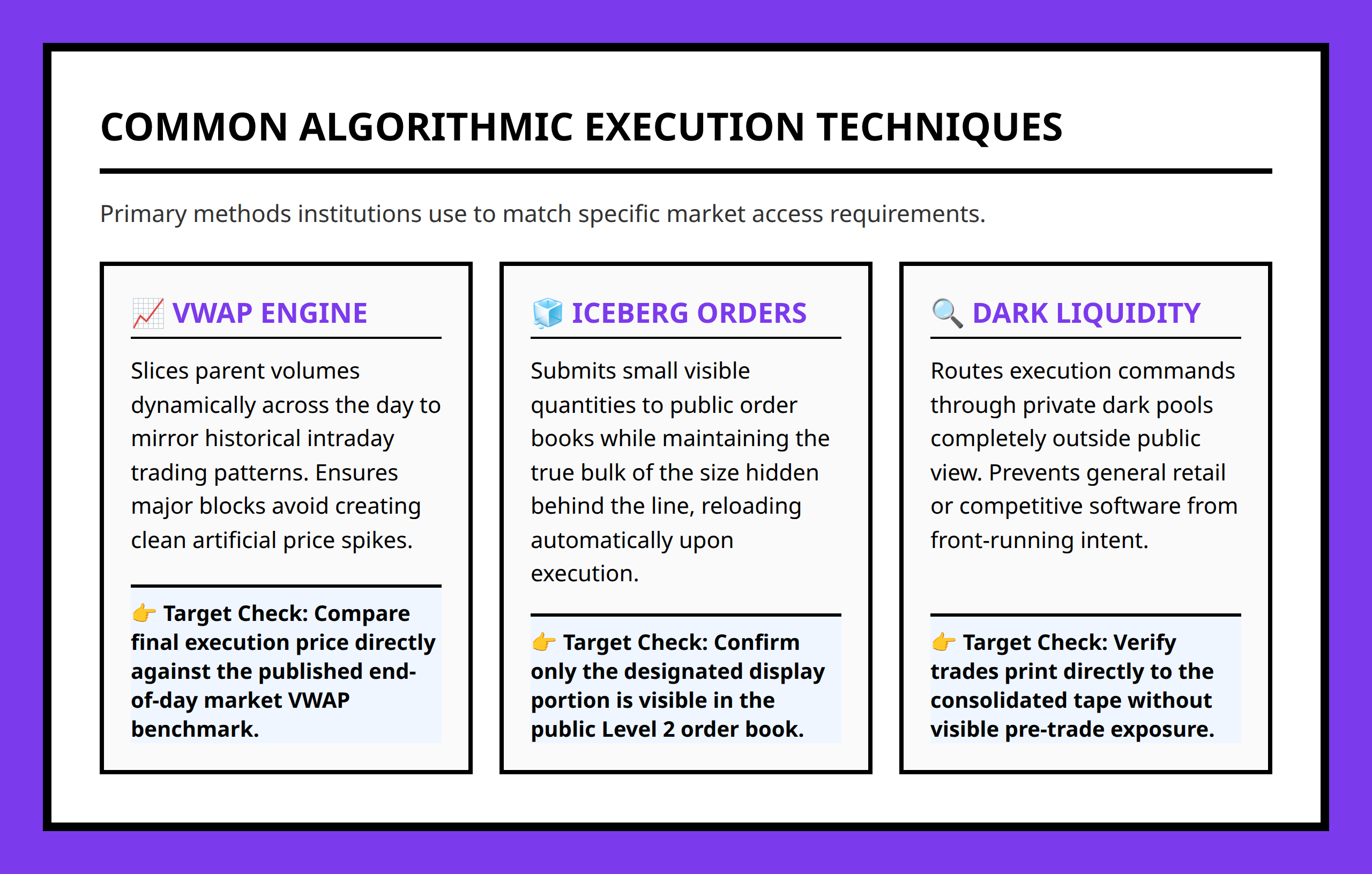

Common Algorithmic Execution Techniques

Different algorithms pursue different execution objectives.

VWAP-Oriented Execution

One common objective is achieving performance relative to volume-weighted market activity.

Rather than completing an order immediately, an algorithm may spread transactions throughout the trading session in a way that aligns execution with overall market volume patterns.

The goal is often to obtain a representative execution outcome while avoiding unnecessary market impact.

Iceberg Orders

Iceberg orders reveal only a portion of the total order size to the market.

The visible portion appears like a normal order. As executions occur, additional hidden quantities become available.

This approach can help preserve anonymity and reduce the likelihood that other market participants identify the true size of the transaction.

Hidden Liquidity and Dark Liquidity

Some execution strategies seek liquidity that is not fully displayed in traditional public quotations.

Accessing hidden liquidity can help institutions complete transactions while limiting information leakage. When fewer market participants can observe a large order, the risk of adverse price reactions may decline.

For large institutional transactions, preserving discretion can be nearly as important as obtaining a favorable price.

Why Execution Algorithms Matter Beyond Speed

Many people assume algorithms exist simply because computers can trade faster than humans.

Speed can matter, but execution quality is usually the more important objective.

Algorithms help balance multiple goals simultaneously. They attempt to manage market impact, locate liquidity, control transaction costs, reduce information leakage, and improve consistency.

In other words, algorithmic trading is often a risk-management process as much as an execution process.

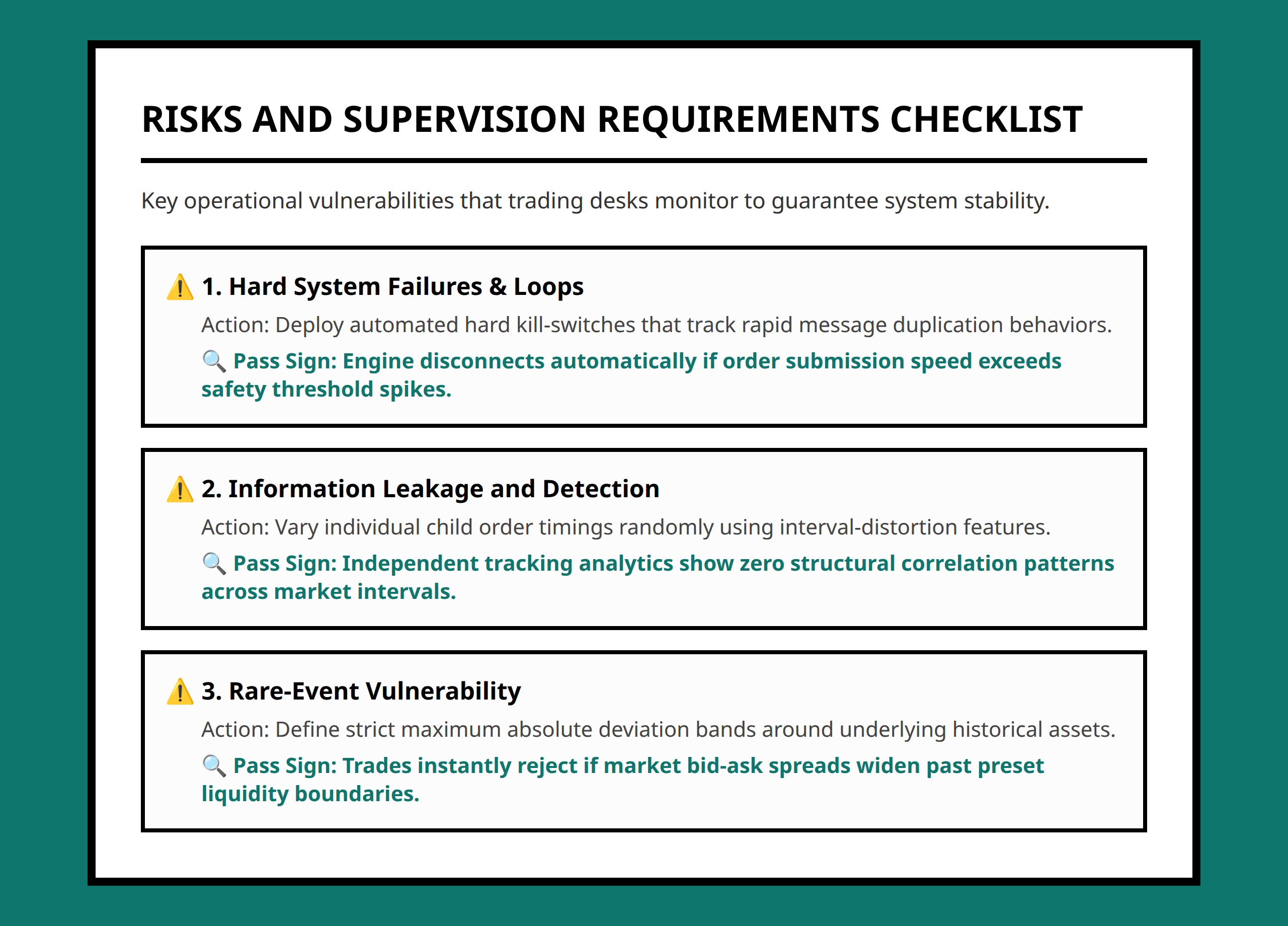

Risks and Limitations of Algorithmic Trading

Algorithmic systems solve important problems, but they introduce their own risks.

System Failures

Execution depends on technology. Hardware failures, software errors, connectivity issues, and configuration mistakes can disrupt trading activity.

Because algorithms operate automatically, robust supervision remains important even when processes are highly automated.

Rare Market Events

Algorithms are designed using assumptions about market behavior. During unusual conditions, those assumptions may not hold.

Unexpected volatility, sudden liquidity shortages, or abnormal trading activity can create challenges that were not anticipated when the algorithm was designed.

Information Leakage

Even when orders are broken into smaller pieces, trading patterns can sometimes reveal information about underlying intentions.

If other participants identify those patterns, the effectiveness of the execution strategy may decline.

This is one reason why execution strategies often combine order slicing, hidden liquidity access, and continuous monitoring.

The Real Purpose of Algorithmic Trading

The most useful way to understand algorithmic trading is to view it as a tool for managing the practical realities of modern markets.

Large orders create challenges involving liquidity, market impact, anonymity, and execution risk. Algorithms help address those challenges by applying predefined rules consistently and efficiently.

Before judging any algorithmic strategy, ask a simple question: is the goal to predict prices, or is the goal to execute trades more effectively? In many institutional settings, execution quality is the primary objective.

FAQ

- Algorithmic Trading: The use of predefined computer-driven rules to execute trades automatically.

- Market Impact: The effect a trade can have on market prices during execution.

- VWAP: An execution objective that relates trading activity to overall market volume patterns.

- Iceberg Order: An order that displays only part of its total size while hiding the remainder.

- Liquidity: The ease with which securities can be bought or sold without significantly affecting prices.

- Execution Risk: The possibility that a trade will not be completed at the expected price or under expected conditions.

- Information Leakage: The unintended disclosure of trading intentions to other market participants.

- Hidden Liquidity: Trading interest that is not fully visible through standard market quotations.