Intrinsic value is the estimated real worth of a business based on its future earning power, not its current market price. Understanding this helps investors judge whether a stock is undervalued, fairly priced, or expensive.

Most investors eventually run into the same problem: a stock looks “cheap” on the surface, but they are not sure if it is actually a good deal. Others see a fast-growing company and assume it must be worth buying, without asking what the business is truly worth underneath the price.

This gap between price and value is where most investing mistakes happen. Intrinsic value investing tries to close that gap by focusing on the actual earning power of a business instead of short-term market movements.

In simple terms, investing becomes much clearer when you stop asking “What is this stock doing today?” and start asking “What is this business worth over time?”

Takeaways

- Intrinsic value focuses on long-term earnings, not short-term price movements.

- A stock price and a business’s true value are often different in the short run.

- Valuation methods like discounted earnings and financial ratios help estimate value.

- Good investing decisions depend more on assumptions than formulas alone.

- Understanding risk and growth expectations is as important as calculating numbers.

What Intrinsic Value Means in Investing

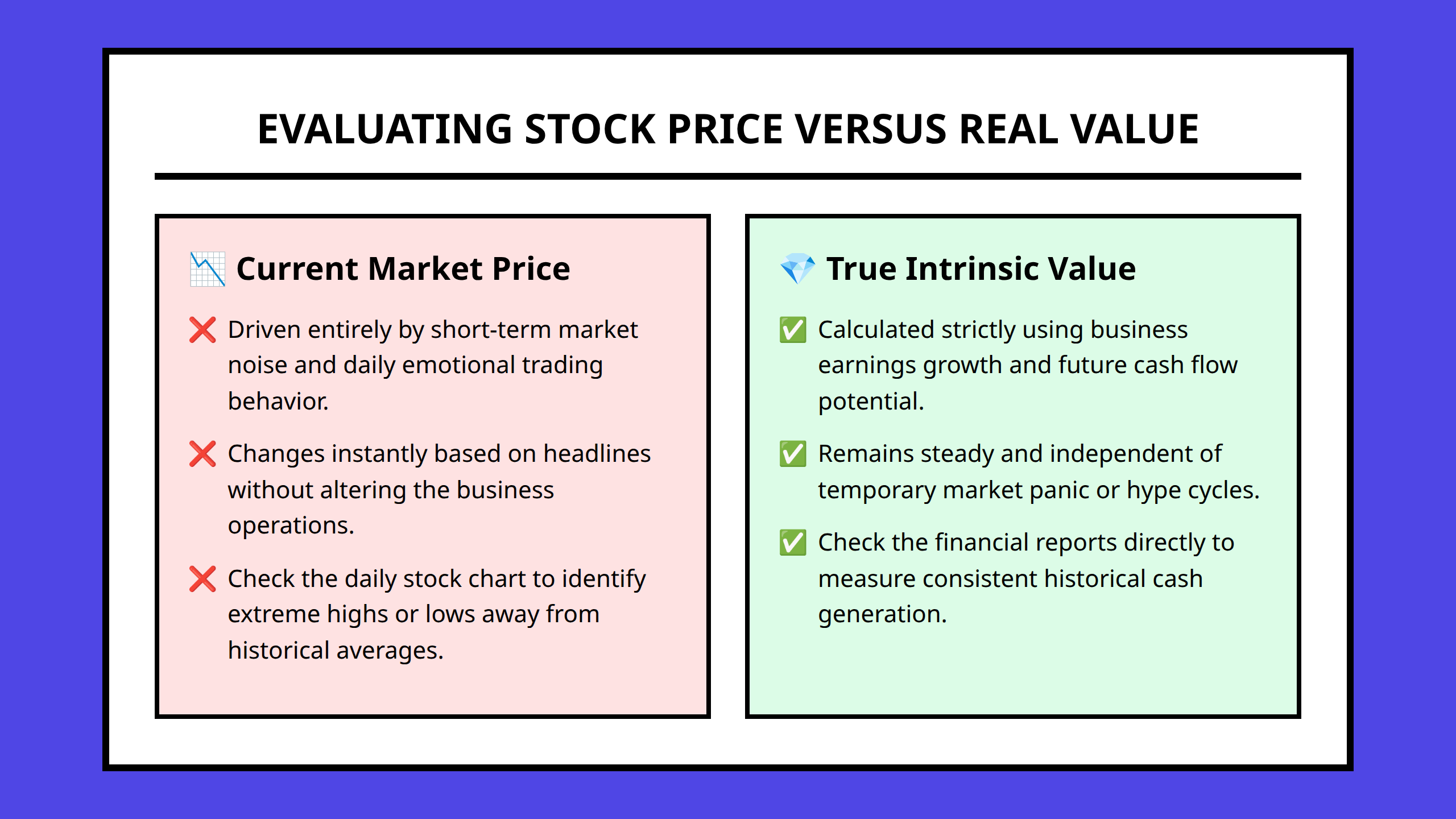

Intrinsic value represents what a business is actually worth based on its ability to generate earnings and cash flow over time. It is not tied to what people are willing to pay for the stock today.

This distinction is important because market prices change constantly. They move based on emotions, news, speculation, and short-term events. Intrinsic value, on the other hand, is based on the long-term economic performance of the business itself.

To understand this better, imagine two layers:

- Market price: The number you see on a stock chart today.

- Intrinsic value: The underlying worth of the business based on its future earnings potential.

These two numbers often move together in the long run, but in the short term they can be very different.

Intrinsic value investing is built on forward-looking analysis. Instead of reacting to what just happened, it tries to estimate what the business will earn in the future and how stable those earnings will be.

At the core, this approach assumes one simple idea: a business is worth the cash it can generate for its owners over time.

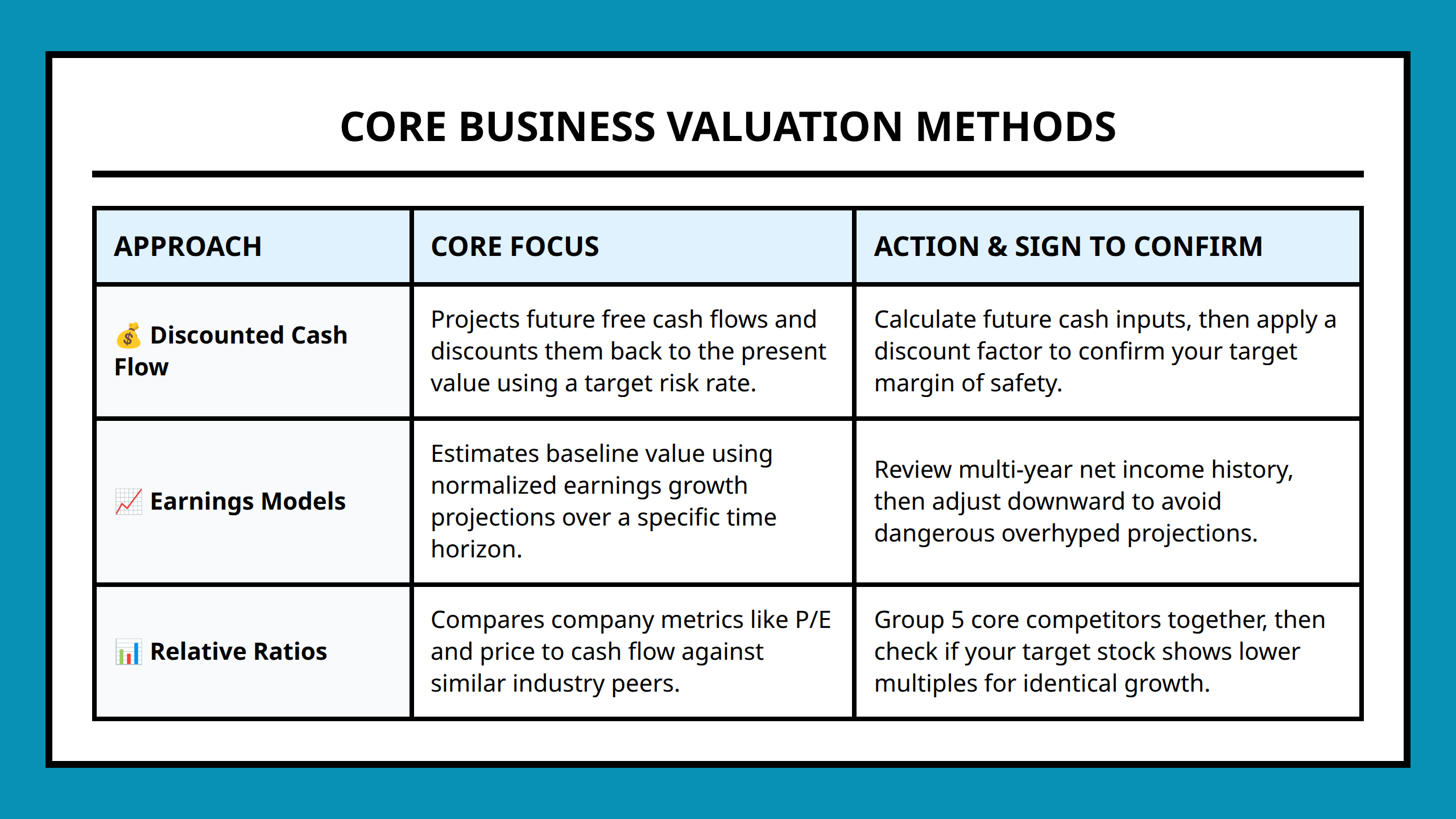

Core Methods for Estimating Business Value

There is no single perfect way to calculate intrinsic value. Instead, investors use different valuation methods to build a reasonable estimate of what a company might be worth.

1. Discounting Future Earnings (Discounted Cash Flow Thinking)

One of the most widely used approaches is based on future earnings. The idea is simple: a business is worth the total amount of money it can generate in the future, adjusted back to today’s value.

This method involves three basic ideas:

- Estimate future earnings or cash flow

- Project how those earnings might grow or stabilize

- Discount them back to today’s value

The logic behind this is that money in the future is worth less than money today because of uncertainty and time.

Even though the math can get complex, the key takeaway is simple: the value of a business depends on how much cash it can reliably produce in the future.

2. Earnings-Based Valuation Models

Another common method focuses directly on earnings. Instead of projecting long cash flow models, investors often look at current earnings and expected growth rates.

For example, a company that earns stable profits each year may be easier to value than one with unpredictable earnings.

This method emphasizes consistency. A business with stable earnings is often easier to estimate than one with highly volatile performance.

3. Relative Valuation Using Ratios

The third method compares a company to others using financial ratios. One of the most common is the P/E ratio (price-to-earnings ratio).

This method does not try to calculate absolute value. Instead, it asks: “How does this company compare to similar businesses?”

Other common ratios include:

- Price-to-cash-flow ratio

- Earnings growth comparisons

- Industry valuation benchmarks

Relative valuation is useful because it gives context. Even a strong business can be overpriced if similar companies are much cheaper.

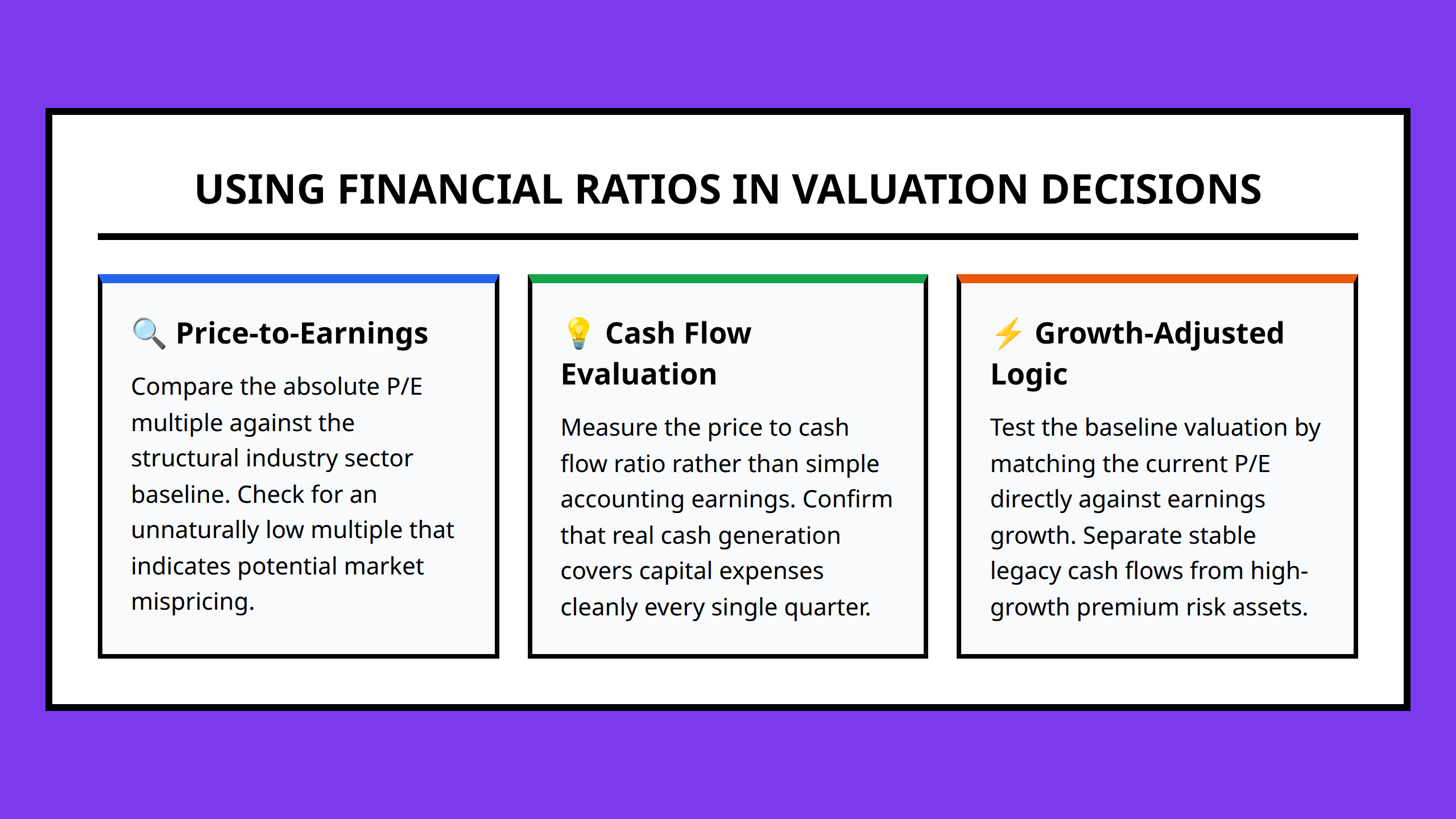

Using Financial Ratios in Valuation Decisions

Financial ratios help translate raw financial data into something comparable and understandable. They are not perfect, but they provide useful signals when combined with deeper analysis.

P/E Ratio and What It Really Tells You

The price-to-earnings ratio shows how much investors are willing to pay for each unit of earnings.

A high P/E ratio often suggests expectations of future growth. A low P/E ratio may suggest slower growth or potential undervaluation—but not always.

What matters most is context. A “cheap” stock is not necessarily a good investment if its earnings are unstable or declining.

Cash Flow and Business Reality

Cash flow often provides a clearer picture than earnings alone. While earnings can be influenced by accounting methods, cash flow reflects actual money entering and leaving the business.

Strong cash flow often signals a healthier and more sustainable business model.

Growth vs Stability Comparison

Valuation also depends heavily on growth expectations.

High-growth companies often appear expensive based on traditional ratios, but investors may accept that price if future earnings are expected to rise significantly.

Stable companies, on the other hand, are often valued based on steady, predictable returns rather than rapid expansion.

The challenge is balancing expectations. Overestimating growth is one of the most common valuation mistakes.

Mistakes That Lead to Wrong Valuation Judgments

Even with the right tools, valuation can go wrong if the underlying assumptions are weak or unrealistic.

Overestimating Growth

One of the most common mistakes is assuming a company will grow faster than it realistically can.

High growth rates often attract attention, but they rarely continue indefinitely. Businesses eventually face competition, market limits, or slowing demand.

When growth expectations are too optimistic, intrinsic value calculations become inflated.

Ignoring Risk and Uncertainty

Another common issue is focusing only on potential returns while ignoring risk.

Two companies might have similar earnings, but one may operate in a stable industry while the other faces unpredictable conditions.

Risk affects value because uncertain cash flows are worth less than stable ones.

Confusing Low Price With Good Value

A low stock price does not automatically mean a company is undervalued.

Sometimes a stock is cheap because the business is declining, facing structural problems, or losing competitive strength.

Value investing requires understanding why the price is low—not just noticing that it is low.

Relying Too Much on One Metric

Valuation mistakes often happen when investors rely on a single ratio or number.

No single metric can fully describe a business. A complete view requires combining earnings, cash flow, growth expectations, and risk.

FAQ

- Intrinsic Value: The estimated true worth of a business based on its future earning power.

- Discounted Cash Flow (DCF): A method that estimates value by projecting future cash flows and adjusting them to today’s value.

- P/E Ratio: A valuation ratio comparing a company’s stock price to its earnings.

- Cash Flow: The actual money a business generates and uses in operations.

- Business Valuation: The process of estimating what a company is worth based on financial performance and expectations.

The most important shift in valuation is not learning formulas, but learning to question assumptions. Before trusting any number, ask what future growth and risk assumptions it depends on. That is often where the real investment decision is made.

A practical next step is simple: choose one company you already follow and compare its current price with a rough estimate of its earnings power. The goal is not precision, but clarity in how you think about value versus price.

References:

- https://www.investopedia.com/terms/i/intrinsicvalue.asp

- https://www.iowaabi.org/news/business-monthly/story/business-valuation-unveiling-the-art-and-science-behind-determining-company-worth/

- https://anderscpa.com/learn/blog/types-of-business-valuation-methods-overview/

- https://financialmodelslab.com/blogs/blog/use-intrinsic-value-method-value-business

- https://www.investopedia.com/terms/v/valuation.asp

- https://keitercpa.com/comprehensive-guide-to-business-valuations/

- https://online.hbs.edu/blog/post/how-to-value-a-company

- https://www.wallstreetprep.com/knowledge/intrinsic-value/

- https://hookagency.com/blog/business-valuation/

- https://www.interactivebrokers.com/campus/trading-lessons/what-is-the-intrinsic-value-of-a-stock/