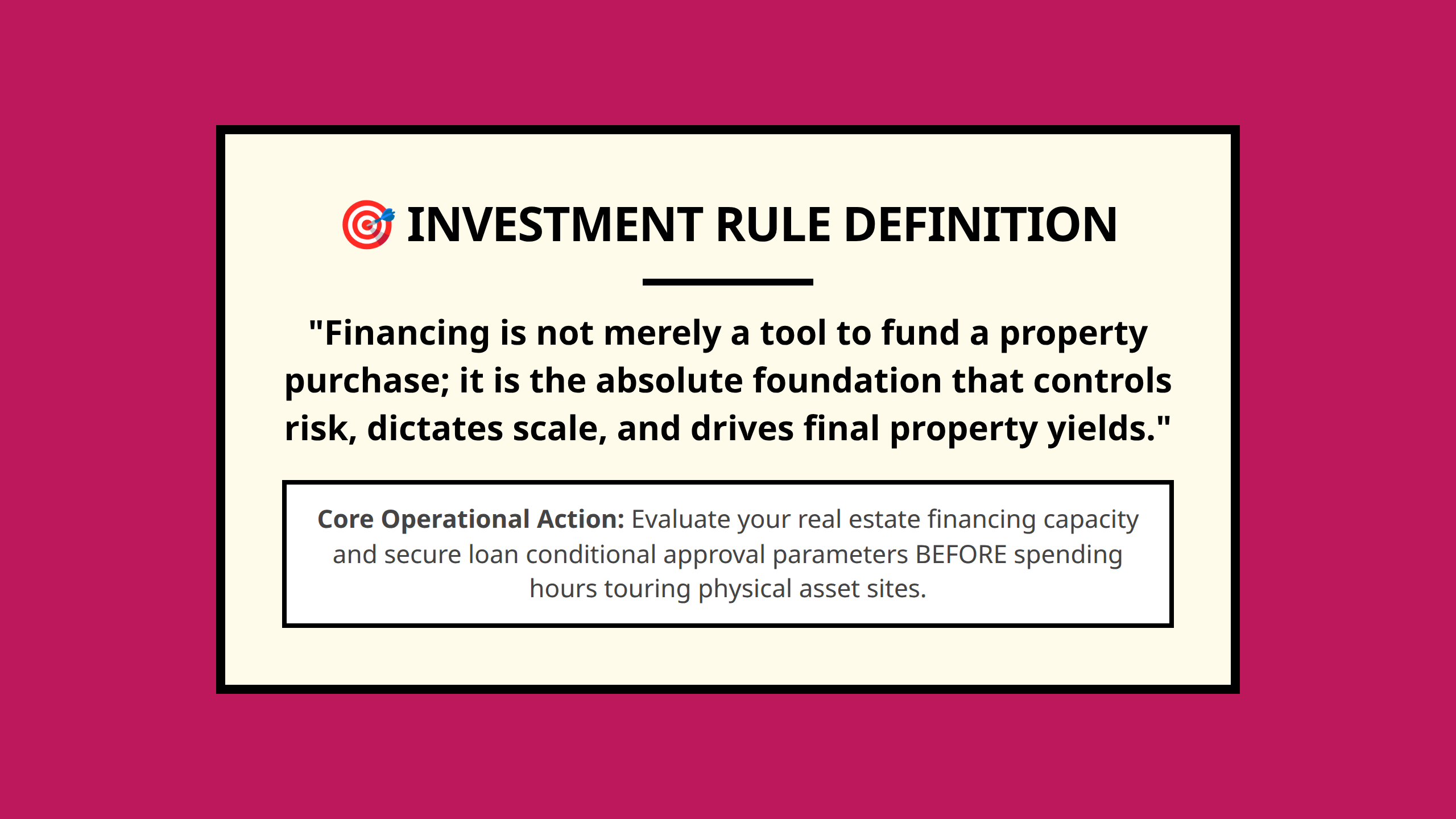

Real estate financing is not just how you pay for a property. It shapes your cash needs, monthly pressure, risk, flexibility, and potential return, so investors should study the financing before judging the deal itself.

Most new property investors start by looking at houses, apartments, or rental income. I would start one step earlier: how the deal will be financed.

The same property can behave very differently under different loan terms. A low down payment may help you buy sooner, but it can also create tighter lender requirements or higher payment pressure. A loan with smaller early payments may feel easier at first, but the later payments still have to be handled.

The best financing strategy matches the loan structure, down payment, borrower qualifications, property type, and investment goal. The point is not to find the fanciest loan. The point is to choose financing that supports the investment instead of quietly working against it.

Takeaways

- Leverage lets investors control real estate with borrowed money, but the payment structure determines how much pressure the investment must carry.

- Loan underwriting usually looks at three things: the borrower, the property, and the location.

- Loan-to-value ratio compares the loan amount with the property value and helps show how much of the purchase is being financed.

- Conventional loans often require stronger qualifications, and lower down payments usually create tougher restrictions.

- Alternative financing can be useful, but it must be judged by cost, control, repayment risk, and exit flexibility.

Why Financing Comes Before the Property Search

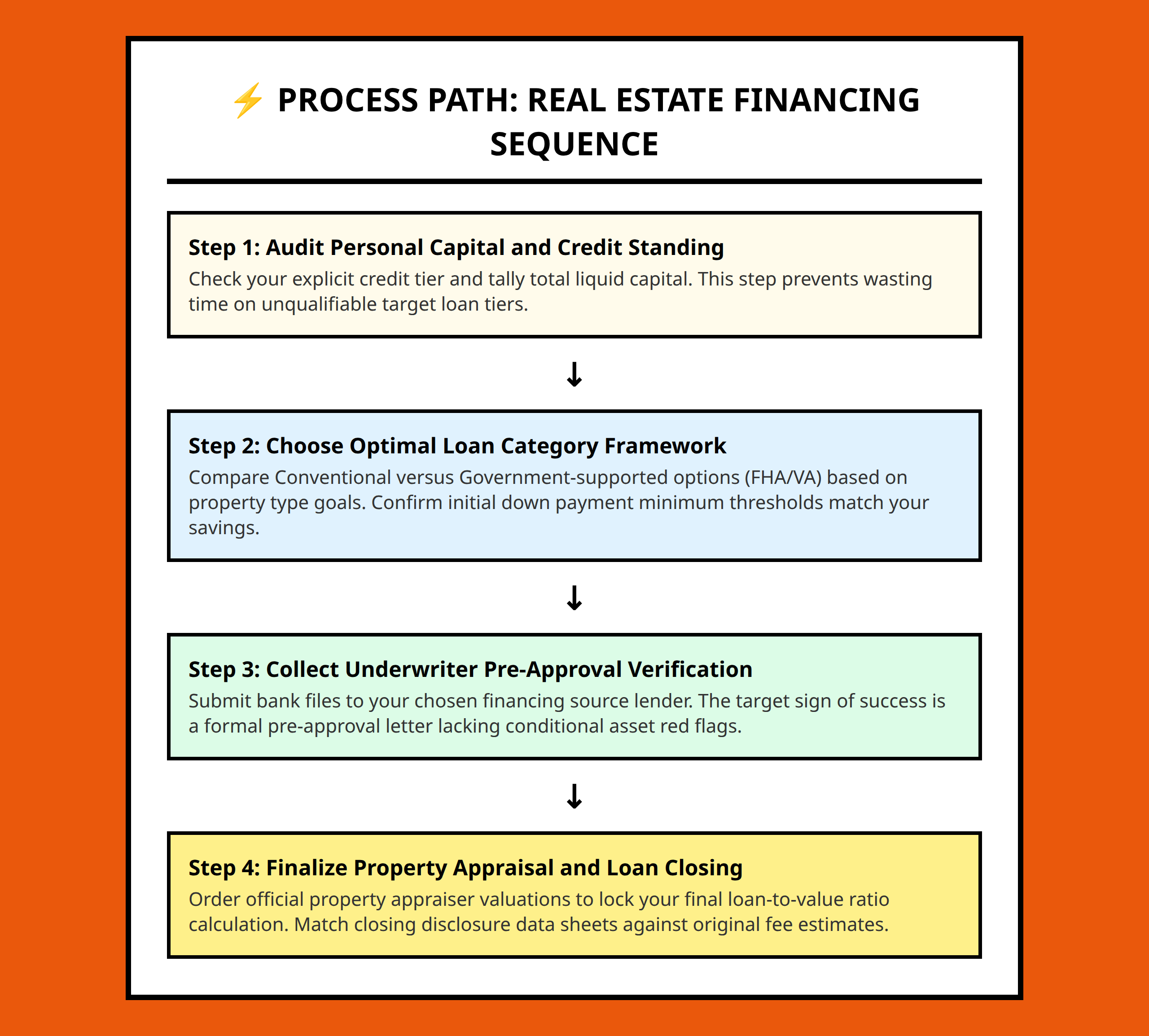

Real estate financing should come before serious property shopping because it defines what kind of deal you can actually complete. It affects the price range, down payment, lender review, closing costs, monthly payments, and future flexibility.

A beginner may see a property and ask, “Can I afford the price?” That question is too narrow. A better question is, “Can this financing structure support the investment plan?”

For example, imagine an investor comparing two modest rental properties. One property has a slightly higher price but straightforward financing and predictable payments. The other has a lower entry cost but a payment schedule that rises later. The cheaper-looking deal may not be safer if the property’s income cannot keep up with future payment pressure.

This is why financing is strategic. It does not simply provide money. It shapes the investor’s room for repairs, vacancy, mistakes, and future decisions.

Understanding Leverage and Loan Fundamentals

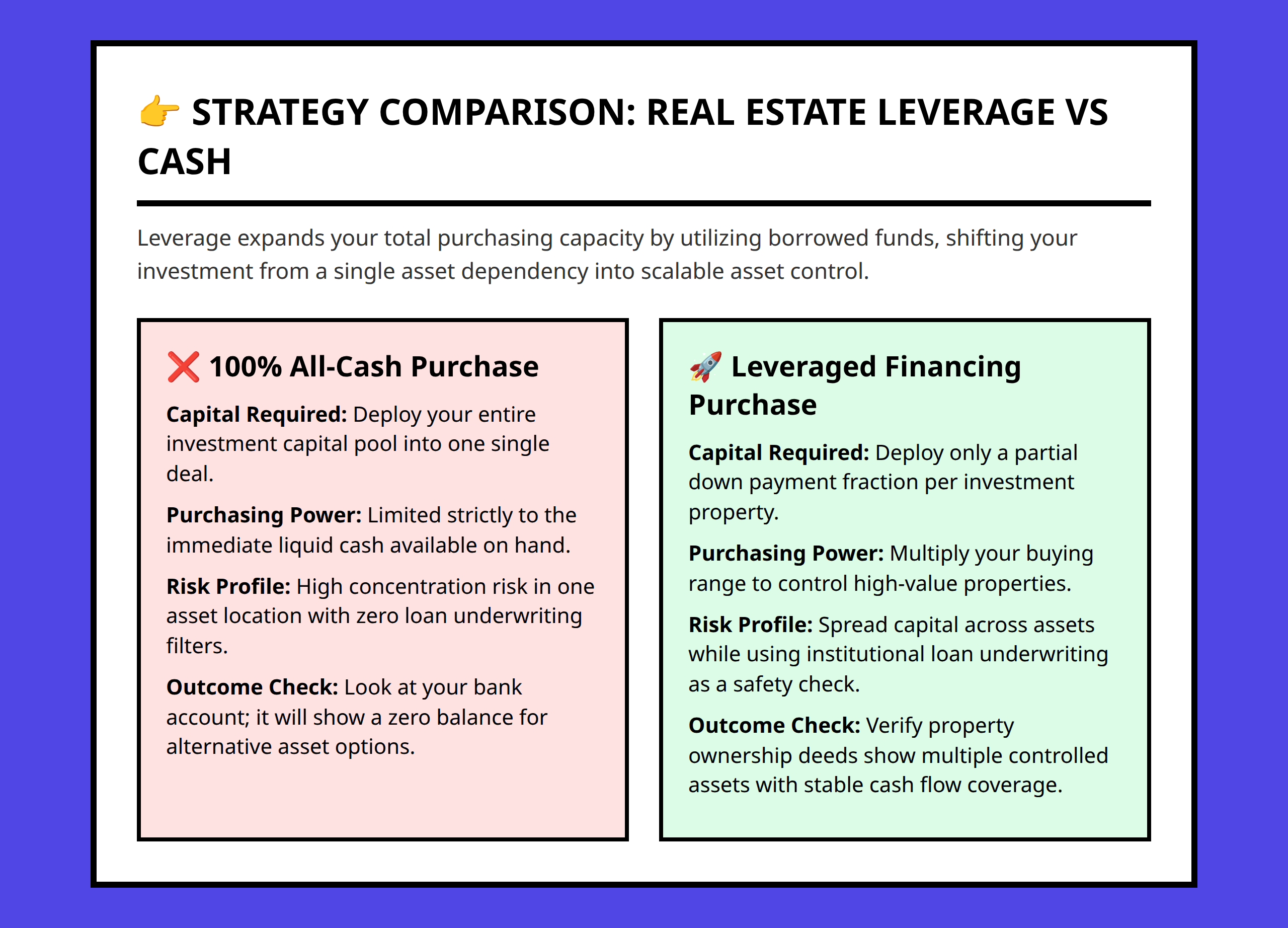

Leverage means using borrowed money to control a larger real estate asset than you could buy with cash alone. It is one of the main reasons real estate attracts investors, but it must be handled with care.

Leverage can increase purchasing power. Instead of waiting until you can pay the full price in cash, financing lets you buy with a portion of the price paid up front and the rest borrowed. That can help an investor begin sooner or acquire a larger property.

But leverage also creates obligations. The loan payment must be made whether the property is vacant, repairs are needed, or rent comes in late. That is why beginners should not treat leverage as free power. It is power with a payment schedule attached.

Several basic loan terms help investors understand what they are agreeing to:

- Interest-only loan: A loan where payments cover interest for a period rather than reducing the principal balance.

- Fully amortized loan: A loan designed so regular payments pay off both interest and principal over the loan term.

- Partially amortized loan: A loan where payments reduce part of the balance, but a remaining balance may still be due later.

- Adjustable-rate loan: A loan where the interest rate can change, creating future payment uncertainty.

- Graduated loan: A loan with smaller early payments that increase over time, based on the expectation that the borrower can handle larger payments later.

The practical test is simple: do not judge a loan only by its first payment. Ask what the loan does over time, how the payments may change, and whether the property can support the obligation.

What Underwriting Really Looks At

Underwriting is the lender’s risk review. It is the process of deciding whether the borrower and property are safe enough for the lender to finance.

A real estate loan can involve a large amount of money, and the lender may be lending money entrusted to it by others. That is why underwriting is not just paperwork. It is a risk check.

The underwriter usually evaluates three basic areas:

- The borrower: Income, financial condition, ability to repay, and credit history.

- The property: The collateral that secures the loan.

- The location: The surrounding area that affects the property’s risk and value.

The borrower typically completes a standard loan application. The lender may review income, financial condition, credit history, and repayment ability. Past due bills, judgments, collection notices, foreclosure, and bankruptcy can all affect how the borrower is viewed.

The lender may also order a credit report and an appraisal. The appraisal matters because the property is the security for the loan. If the borrower fails to repay, the lender wants confidence that the property has enough value to protect the loan.

For beginners, this creates a useful mindset shift. You are not only trying to like the property. You are trying to see whether the borrower, property, and location make sense together.

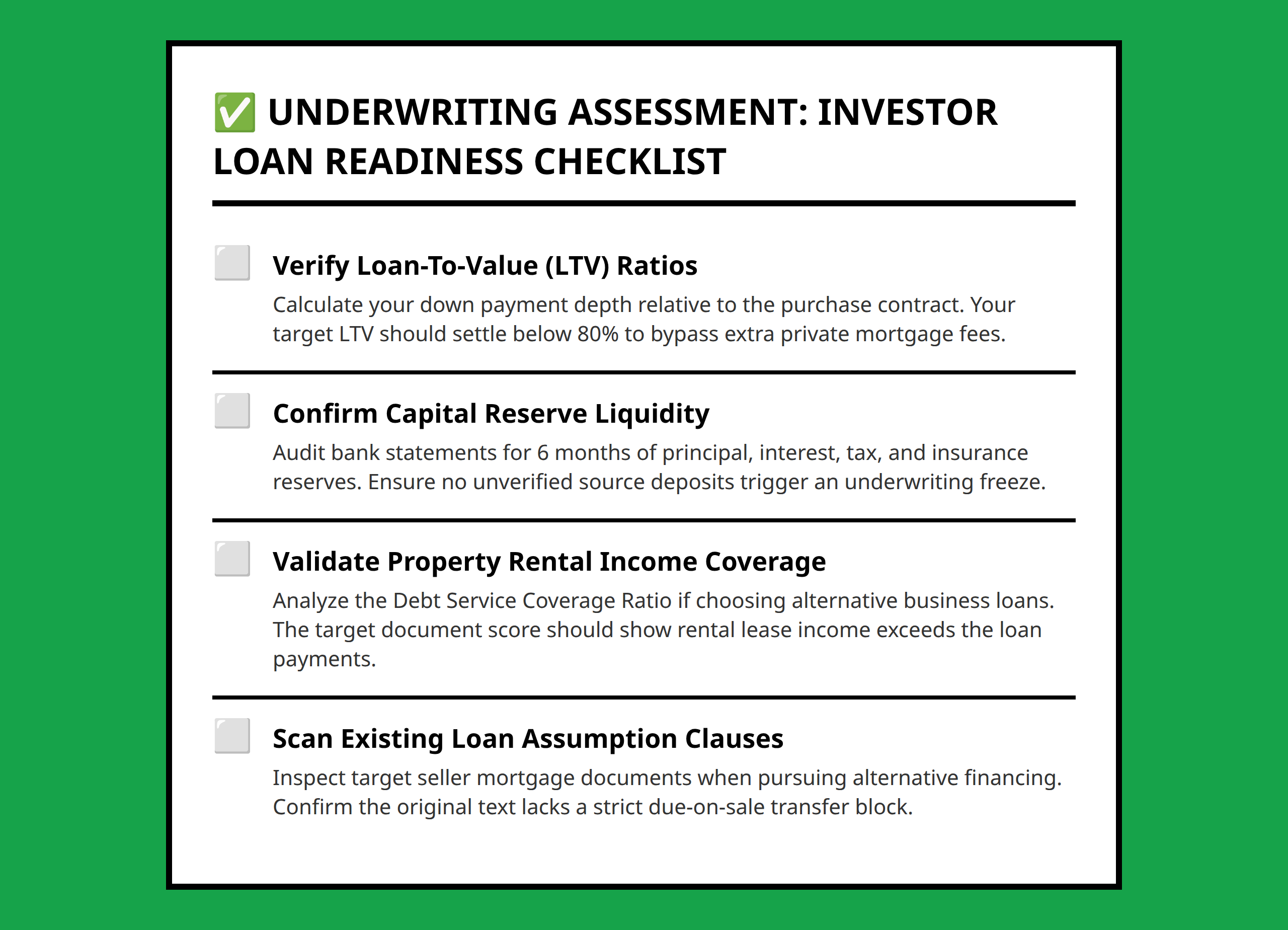

Loan-to-Value Ratio: The Number Beginners Should Not Skip

Loan-to-value ratio, often called LTV, compares the loan amount with the property value. It helps show how much of the property is being financed and how much equity or down payment is involved.

If a property has a high loan-to-value ratio, more of the purchase is being financed. That may preserve cash up front, but it can also mean more lender risk and tighter requirements. If the loan-to-value ratio is lower, the investor usually has more equity in the property from the start.

This matters because down payment and qualification requirements often move together. With conventional financing, lower down payments usually come with tougher restrictions. A conventional loan commonly requires a substantial down payment, and when the down payment is below that level, private mortgage insurance may be required to protect the lender from default.

Beginners should use LTV as a reality check. A deal may sound attractive because it requires less cash up front, but the investor still needs to ask:

- How much debt will the property carry?

- Will the payment fit the rental or resale plan?

- What extra costs appear because of the lower down payment?

- How much room remains for repairs, closing costs, and vacancy?

The goal is not always the lowest possible down payment. The goal is a financing structure that gives the investment enough breathing room.

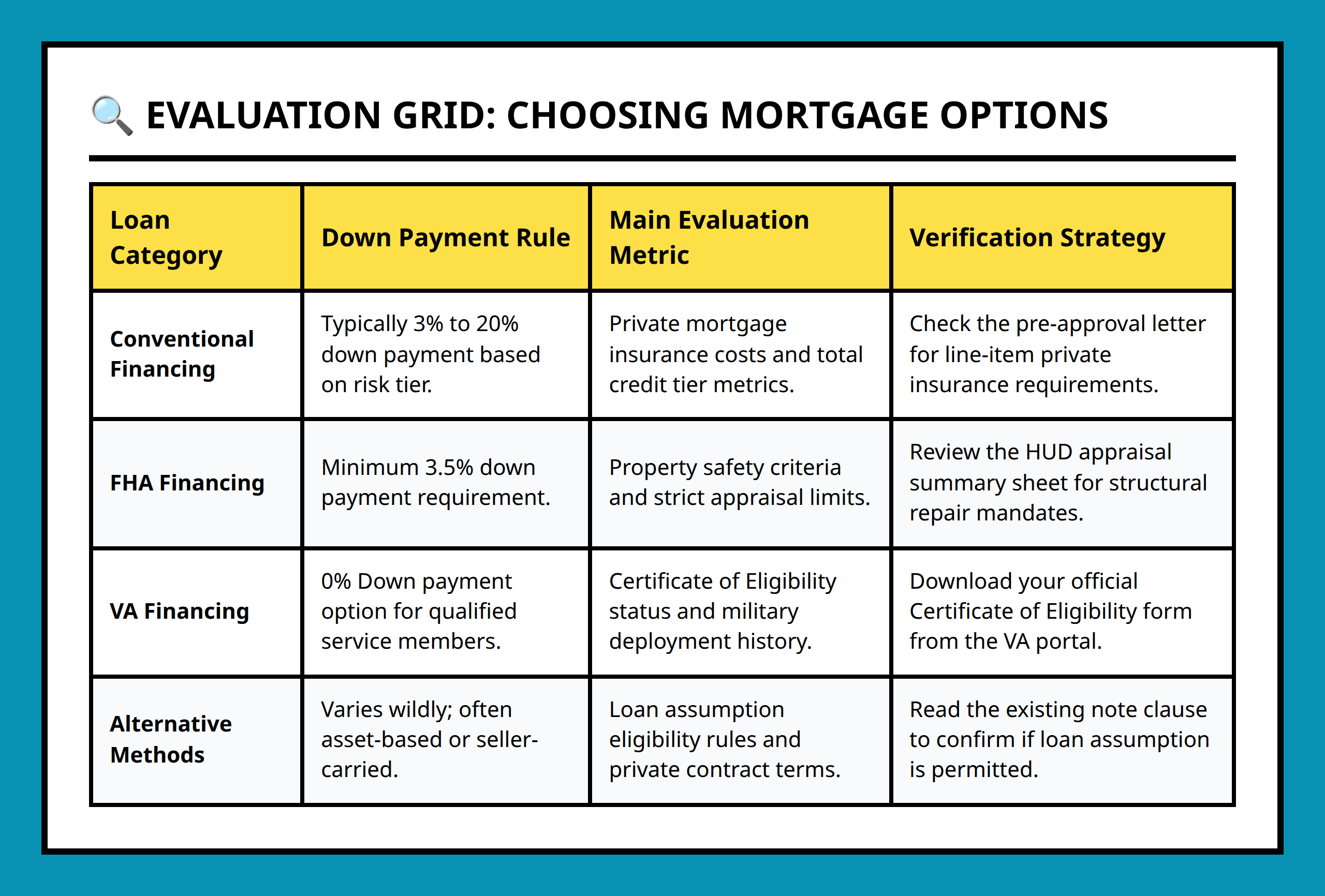

Comparing Major Real Estate Financing Options

The main financing options differ by who they serve, how they qualify borrowers, and what kinds of properties or limits they involve. A beginner should compare them by fit, not by name recognition.

| Financing option | How it generally works | What investors should notice |

|---|---|---|

| VA financing | Loans for eligible veterans, with private lenders involved and the Veterans’ Administration guaranteeing qualifying loans. | Eligibility, property type, appraisal, entitlement, occupancy requirements, closing costs, and points all matter. |

| FHA financing | Government-backed loan insurance designed to support lending and uniform qualification standards. | Program rules, property type, loan limits, insurance, points, and occupancy rules may affect fit. |

| Conventional financing | Financing outside FHA and VA programs, commonly used by non-veterans or borrowers seeking amounts beyond FHA limits. | Qualification standards can be stricter, and lower down payments usually bring tougher restrictions. |

| Loan assumption | A buyer takes over an existing loan under allowable terms. | Assuming a favorable existing loan can be less cumbersome than creating new financing, but qualification rules may apply. |

| Seller or alternative financing | Financing may involve the seller, second mortgages, land contracts, equity sharing, personal loans, or related structures. | Terms must be clear, written, and evaluated for repayment risk and control. |

VA financing is designed around eligible veterans and can apply to property types such as one- to four-family dwellings, single-family dwellings including condominiums, mobile homes, and mobile home lots. The process includes eligibility, application, appraised value, loan guaranty, buyer qualification, down payment, existing loans, entitlement, occupancy requirement, closing costs, points, and impounds.

FHA financing has a different role. It helped establish loan insurance and more uniform qualification standards. FHA-related programs can apply to different property types and purposes, including one- to four-family housing, multifamily dwellings, condominiums, mobile homes, rehabilitation, and certain lower-income housing programs.

Conventional financing is the main path beyond FHA and VA programs. It is especially relevant for non-veterans and borrowers who want to borrow more than FHA limits allow. It usually has stricter qualification requirements, and the lower the down payment, the tougher the restrictions tend to become.

Discount Points, Service Points, and Why Interest Rate Is Not the Whole Cost

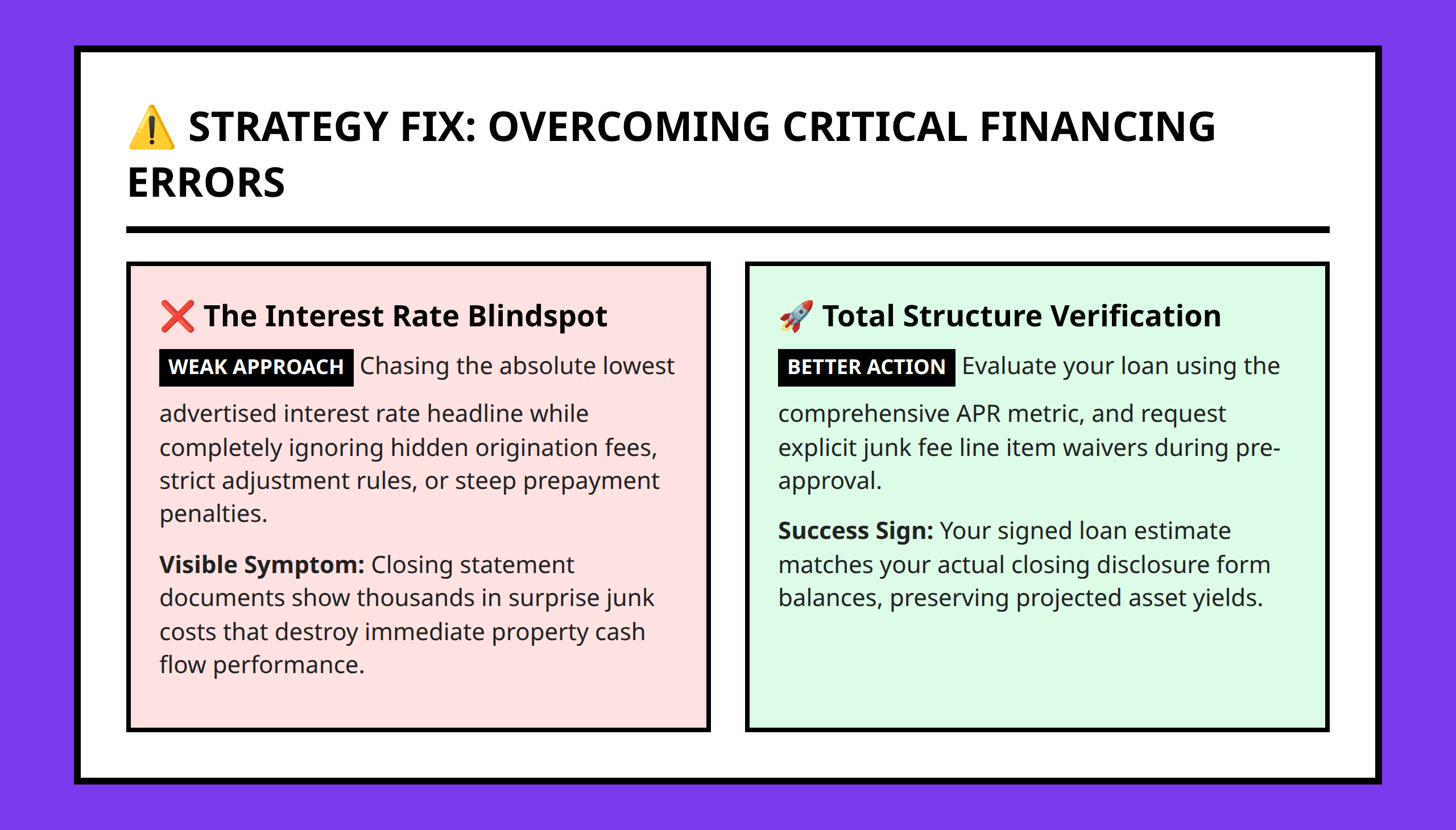

Interest rate matters, but it is not the only cost in a loan. Points can change the real price of financing.

A discount point generally represents a percentage of the loan amount. In certain VA and FHA contexts, discount points can be used to make a loan more attractive to lenders when there is a difference between a fixed program rate and open market rates. Service points, often called loan origination fees, may also be charged to increase the lender’s yield without raising the interest rate.

This is where beginners should be careful. A loan can look appealing because the rate seems reasonable, but points and fees still affect the total cost. The useful question is not only, “What is the rate?” It is also, “What must be paid to get this loan?”

A practical comparison worksheet should include at least these items:

- Interest rate

- Loan amount

- Down payment

- Discount points

- Service points or origination fees

- Closing costs

- Mortgage insurance, if required

- Whether the payment can change later

Looking at these items together helps prevent one of the most common beginner mistakes: choosing the loan that sounds cheapest before understanding the full financing package.

Alternative Financing Methods Can Help, but They Need Structure

Alternative financing can be useful when conventional lending does not fit the deal, but it should never be treated casually. These methods can create flexibility, yet they also require clear terms and careful risk judgment.

Examples of alternative real estate financing include wrap-around mortgages, land contracts, equity loans, purchase-money seconds, take-out seconds, equity sharing, chattel loans, and personal loans.

A purchase-money second, for example, may help complete a purchase when the first loan does not cover enough of the price. A land contract may structure the sale differently from a standard mortgage transaction. Equity sharing may involve splitting ownership or benefit in a way that must be clearly understood by all parties.

For a beginner, the practical standard is this: if the financing structure is hard to explain in plain English, slow down before signing anything.

Ask:

- Who is lending the money?

- Who holds title or security?

- When are payments due?

- What happens if payments are missed?

- Can the property be sold or refinanced later?

- Are all terms in writing?

Alternative financing is not automatically better or worse than conventional financing. It is simply more dependent on structure, clarity, and discipline.

Where Real Estate Financing Can Come From

Funding sources matter because different lenders prefer different loan types, property types, and time frames. The right source depends on the investment plan.

Real estate financing can come from existing property sellers, savings and loan associations, commercial banks, credit unions, insurance companies, limited partnerships, loan brokers, and the secondary mortgage market.

Each source tends to have its own role:

- Existing property sellers: May help create financing directly as part of the sale.

- Savings and loan associations: Traditionally connected with residential real estate financing.

- Commercial banks: Often prefer shorter-term financing.

- Credit unions: Can be useful for take-out second mortgage loans, personal loans, vehicle loans, and some intermediate secured real estate loans.

- Insurance companies: Often focus on larger-scale commercial lending and may seek higher yields or equity participation.

- Limited partnerships: Can help finance investments beyond one investor’s personal financial ability by pooling capital.

- Loan brokers: May help locate financing sources.

- Secondary mortgage market: Helps move mortgage loans through larger financial channels.

Limited partnerships deserve special care. They may allow a real estate project to move forward when one person does not have enough capital alone. But the roles should be clear: limited partners are usually investors only, while the general partner manages the property. Major decisions, such as selling or refinancing, should be handled according to the partnership structure, and buy-out options can help protect the partnership’s survival.

That is a good reminder for all financing: the money source is never just money. It comes with expectations, control issues, timing, and obligations.

Common Financing Mistakes Investors Make

The biggest financing mistakes happen when investors chase approval instead of fit. Getting a loan is not the same as choosing a good financing structure.

- Focusing only on the interest rate: Points, service fees, insurance, closing costs, and future payment changes can matter just as much.

- Ignoring underwriting: Lenders evaluate the borrower, property, and location. A weak point in any one of these can slow or block financing.

- Assuming low down payment is always better: Less cash up front can create stricter qualification requirements or extra costs.

- Overlooking loan assumption: Existing favorable loans can sometimes be valuable, but assumptions must be checked for rules and qualification requirements.

- Using alternative financing without written clarity: Flexible structures need clear terms, responsibilities, and default rules.

- Choosing a loan before defining the investment goal: A short-term resale plan, long-term rental plan, and development plan may each need different financing.

A useful habit is to compare financing options before comparing properties. That may feel slower at first, but it keeps you from falling in love with a deal that your financing cannot safely support.

FAQ

- Real estate financing: The methods and sources used to fund a property purchase, refinance, construction project, or investment deal.

- Leverage: Using borrowed money to control a larger real estate asset than cash alone would allow.

- Mortgage: A financing arrangement where real estate serves as security for repayment of the loan.

- Loan-to-value ratio: A comparison between the loan amount and the property value, used to judge how much of the property is financed.

- Underwriting: The lender’s risk review of the borrower, property, and location before approving a loan.

- Interest-only loan: A loan where payments cover interest for a period without reducing the principal balance.

- Fully amortized loan: A loan structured so regular payments pay off both interest and principal over the loan term.

- Adjustable-rate loan: A loan where the interest rate can change, which may cause payment changes later.

- Graduated loan: A loan with smaller early payments that increase over time.

- Discount points: Charges based on a percentage of the loan amount, often used to affect lender yield or loan pricing.

- Service points: Loan origination fees that may be charged as a percentage of the loan amount.

- Loan assumption: Taking over an existing loan under allowable terms instead of creating entirely new financing.

- FHA financing: Financing connected with Federal Housing Administration loan insurance and program rules.

- VA financing: Financing for eligible veterans, with the Veterans’ Administration guaranteeing qualifying loans made by private lenders.

- Conventional financing: Real estate financing outside FHA and VA programs, often with stricter qualification standards.

- Private mortgage insurance: Insurance used to protect the lender when a conventional loan has a lower down payment.

- Purchase-money second: A second loan used as part of the purchase financing when the first loan does not cover the full needed amount.

- Equity sharing: A financing arrangement where parties share ownership benefits or future value under agreed terms.

Before evaluating your next property, make a simple financing worksheet with the loan type, down payment, LTV, payment structure, points, closing costs, qualification issues, and exit flexibility. If the financing does not make sense on one page, the property is not ready for a decision.