A long-term investment strategy works best when it is built around economic reality rather than market excitement. Understanding inflation, risk, economic cycles, and diversification can help investors make decisions that remain effective even when conditions change.

One of the easiest mistakes investors make is focusing entirely on a specific investment while paying little attention to the environment surrounding it. A great investment idea at the wrong time can produce disappointing results. Meanwhile, an ordinary investment chosen with a clear understanding of economic conditions may perform much better over the long run.

I find that many investing discussions focus on what to buy. The more important question is often why a particular investment fits the economic conditions you expect to face. Long-term success usually comes from matching investments to reality rather than trying to predict the next exciting opportunity.

Takeaways

- The economy influences investment results more than many investors realize.

- Inflation can quietly reduce the real value of investment gains.

- Higher potential returns almost always come with higher risk.

- Diversification helps reduce dependence on a single economic outcome.

- A balanced strategy is often more durable than an aggressive prediction about the future.

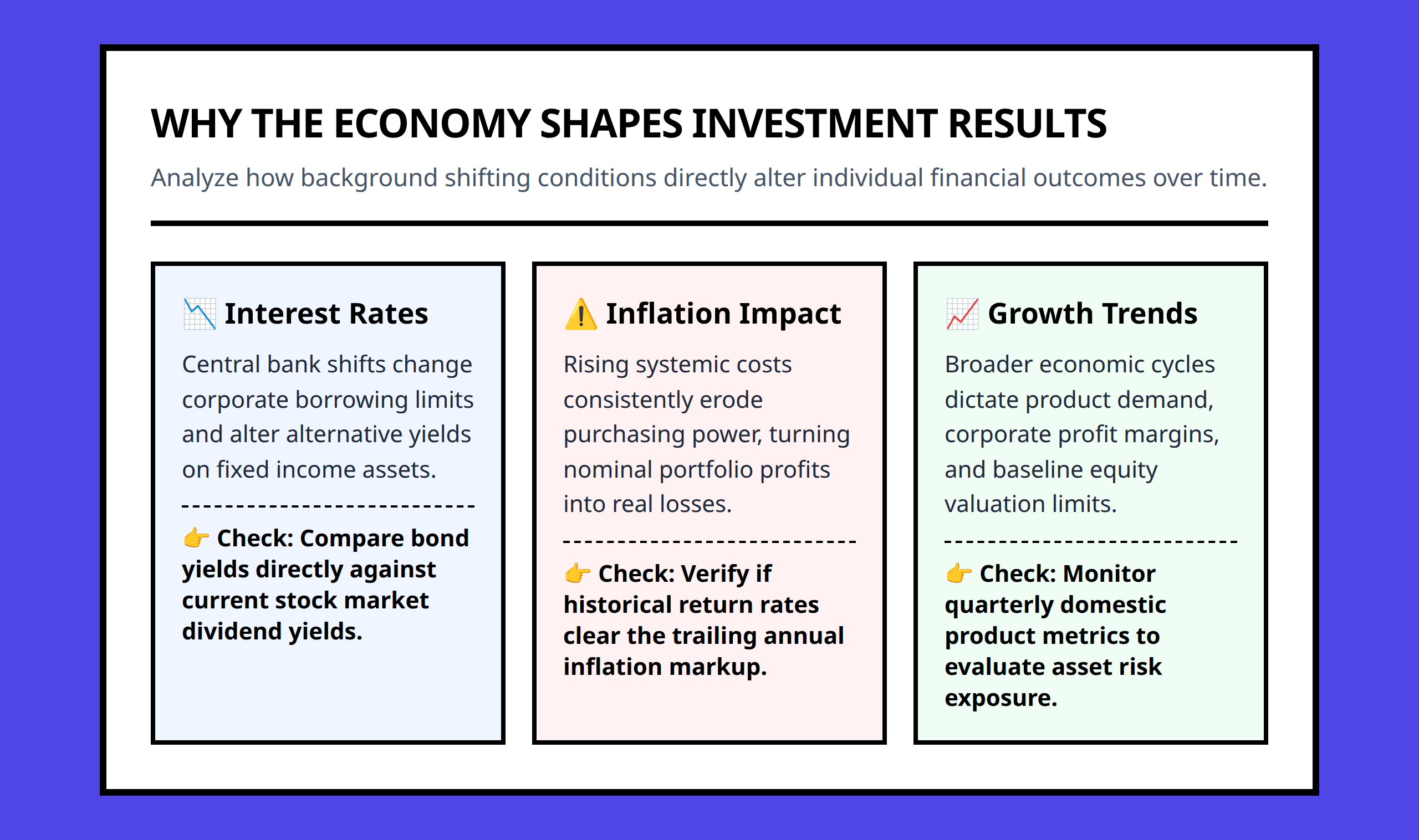

Why the Economy Shapes Investment Results

The economy affects nearly every investment decision. Businesses grow or struggle within economic conditions, consumers spend more or less depending on confidence and income, and inflation changes what money can actually buy.

Many investors focus on nominal gains while overlooking purchasing power. A portfolio may appear to grow significantly over time, but if inflation rises faster than expected, the real value of those gains can be much lower.

Consider a simple illustration. An investor may see an account increase substantially over several decades and assume that wealth has grown dramatically. However, if the cost of housing, transportation, and everyday goods rises sharply during the same period, much of that apparent gain may simply reflect inflation.

This is why understanding economic trends matters. Investment results cannot be evaluated in isolation. They must be viewed alongside the broader forces affecting purchasing power and financial security.

Building an Investment Strategy Around Economic Trends

A durable investment strategy starts with recognizing that economic conditions change. Inflation, recessions, recoveries, and periods of rapid growth all influence how investments perform.

Instead of reacting to short-term headlines, investors are often better served by focusing on long-term trends. Economic shifts usually develop over years rather than weeks. Looking beyond daily market movements helps create a more stable decision-making process.

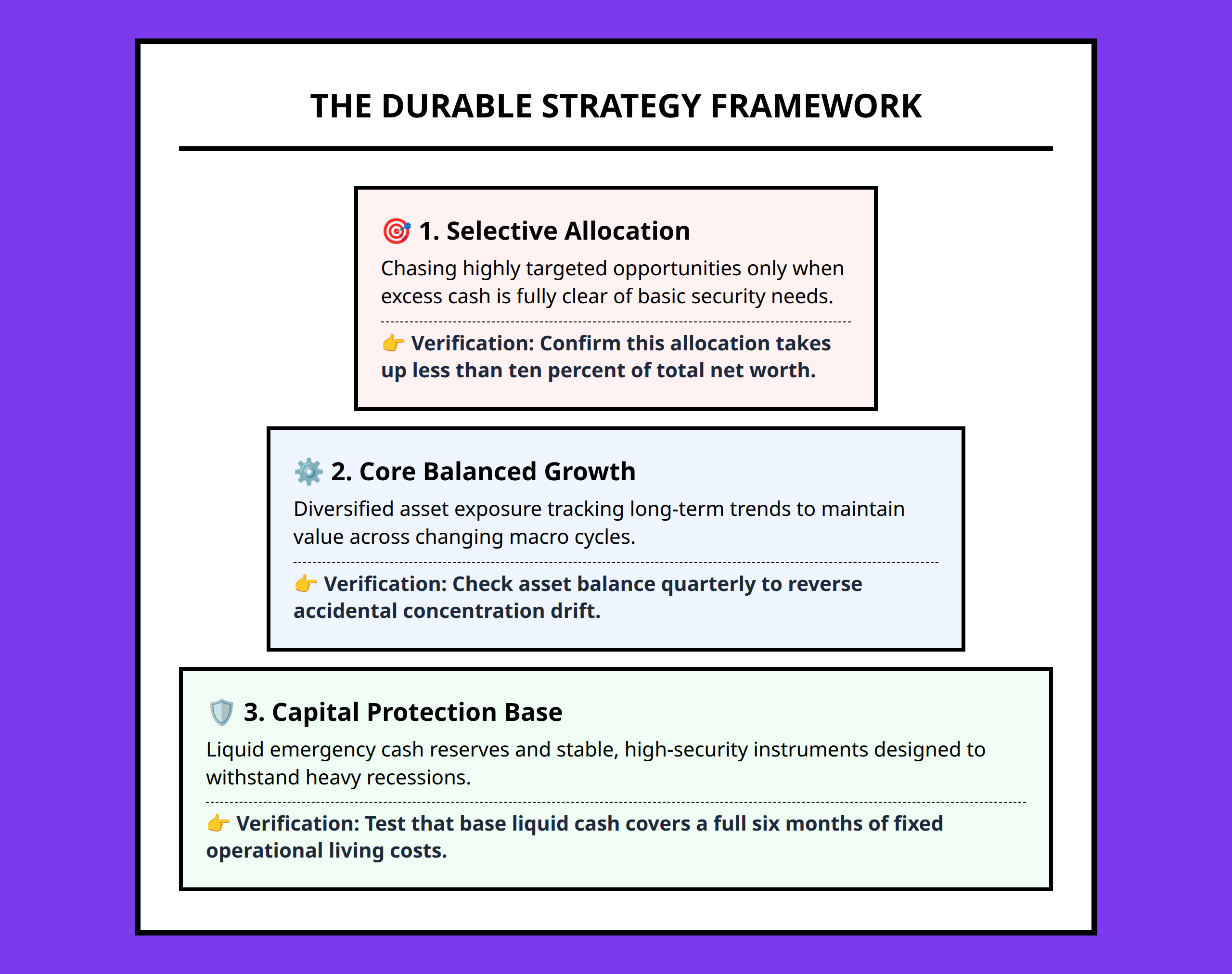

One practical approach is balancing growth opportunities with capital protection. No one can predict the future with complete accuracy. Because of that uncertainty, building a portfolio around a single economic prediction can be dangerous.

A balanced framework might look like this:

| Investment Goal | Primary Focus | Role in Strategy |

|---|---|---|

| Growth | Long-term appreciation | Build future wealth |

| Income | Steady returns | Support financial stability |

| Capital Protection | Preserving principal | Reduce downside risk |

| Diversification | Multiple asset categories | Avoid concentration risk |

The key idea is not to guess every economic turn correctly. The goal is to remain positioned to survive and adapt regardless of which scenario unfolds.

For example, imagine two investors. One commits nearly everything to a single economic prediction. The other spreads investments across several categories while maintaining a clear focus on risk management. If the future unfolds differently than expected, the second investor is usually in a stronger position to recover and continue building wealth.

The Critical Role of Inflation in Long-Term Investing

Inflation deserves special attention because it quietly affects every long-term plan.

Many people think about investment returns but spend less time considering what those returns will actually buy in the future. An investment that doubles may seem impressive, but the result becomes less meaningful if the cost of living rises dramatically during the same period.

This is why investors should evaluate performance in terms of purchasing power rather than account balances alone.

When building a long-term investment strategy, ask a simple question: will this investment help preserve or improve purchasing power over time?

That question often leads to better decisions than focusing exclusively on stated returns.

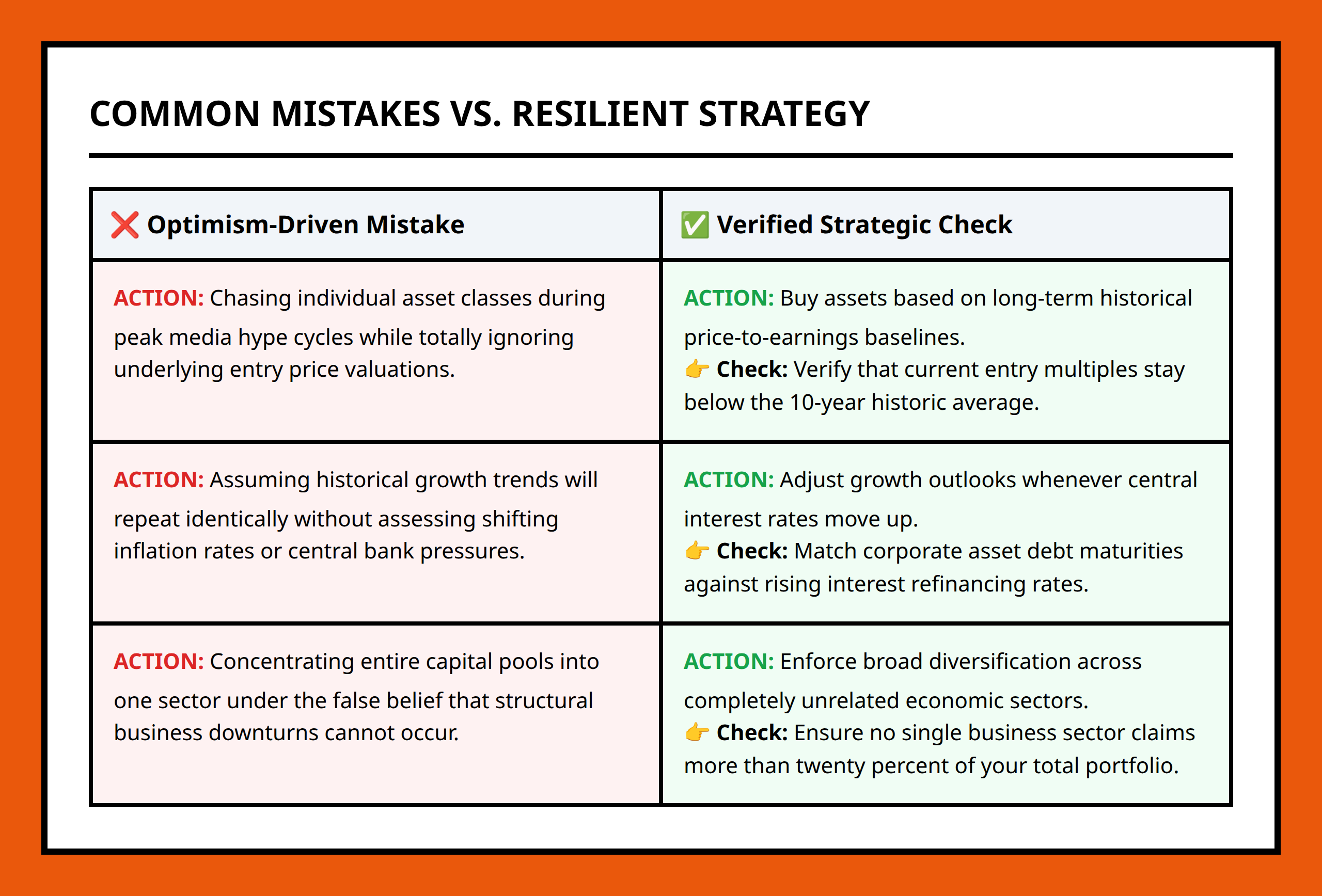

Common Mistakes Investors Make

The most common investing mistakes tend to repeat across generations even when the specific investments change.

Ignoring the Relationship Between Risk and Return

A fundamental investing principle is that higher potential returns generally come with higher risk. Temporary market conditions can sometimes make this relationship appear less important, but over time the connection usually reasserts itself.

When a promised return appears unusually attractive, it is wise to ask what risks are being accepted in exchange for that opportunity.

Following Optimism Instead of Analysis

Many poor investment decisions begin with excitement rather than careful evaluation. Investors often assume favorable conditions will continue indefinitely.

Economic cycles eventually change. Investments that appear unstoppable during strong periods may become vulnerable when conditions reverse.

Concentrating Too Much in One Idea

Some investors place excessive confidence in a single company, sector, or prediction about the future.

Diversification exists because uncertainty exists. Spreading investments across multiple categories can reduce the damage caused by any one mistake.

Ignoring Personal Circumstances

Investment strategies should reflect life stage, goals, and financial needs. Someone focused on long-term growth may reasonably approach investing differently from someone approaching retirement who needs greater protection of existing assets.

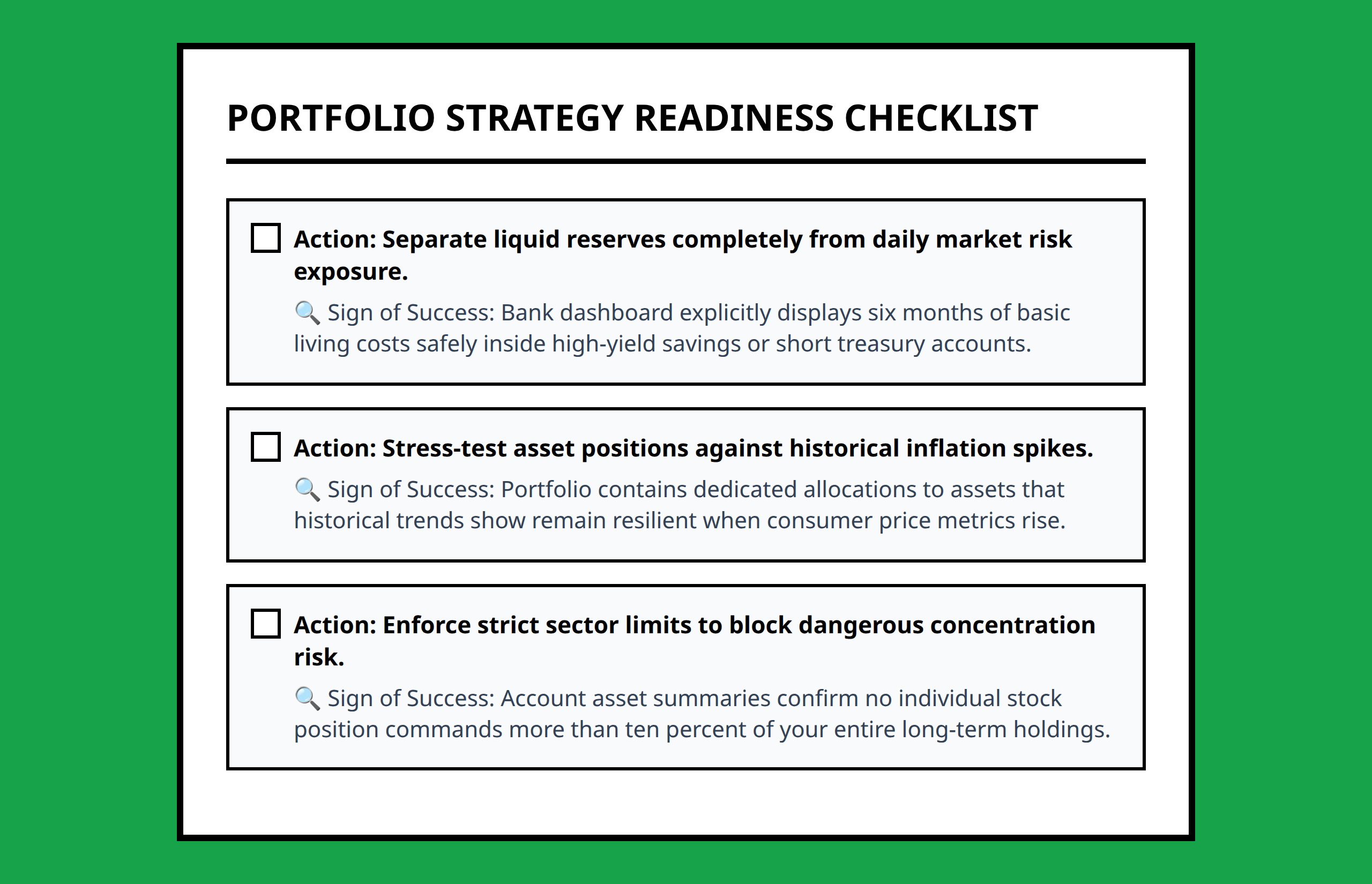

Building a Resilient Long-Term Investment Framework

A resilient strategy does not require perfect economic forecasts.

Instead, it requires a disciplined approach built on a few durable principles:

- Understand the economic environment.

- Pay attention to inflation and purchasing power.

- Respect the relationship between risk and return.

- Diversify rather than depend on a single outcome.

- Adjust strategy as personal circumstances change.

- Focus on long-term trends rather than short-term noise.

Investors often feel pressure to predict what happens next. In reality, long-term success frequently comes from preparing for multiple possibilities instead of betting everything on one forecast.

FAQ

- Inflation: The gradual increase in prices over time, which reduces the purchasing power of money.

- Diversification: Spreading investments across multiple categories to reduce concentration risk.

- Capital Protection: Strategies designed to preserve existing assets and reduce the likelihood of major losses.

- Recession: A period of economic slowdown typically associated with reduced spending and weaker business activity.

- Risk and Return: The principle that investments offering higher potential rewards usually involve higher levels of uncertainty and possible loss.

- Purchasing Power: The amount of goods and services that money can buy at a given time.

The strongest long-term investment strategy is usually not the one built on the most confident prediction. It is the one built to endure uncertainty. Before making your next investment decision, review whether your portfolio is prepared for more than one economic outcome—not just the one you hope will happen.