Implied Volatility vs Realized Volatility is one of the most important concepts in volatility investing. Historical volatility measures past price movement, implied volatility reflects market expectations, and realized volatility shows what actually happens. Understanding the relationship between all three helps investors evaluate risk more effectively.

Volatility terminology often sounds more complicated than it really is. Many investors encounter phrases like implied volatility, realized volatility, and historical volatility and assume they are describing the same thing.

They are closely related, but they answer different questions. One looks backward, one reflects expectations about the future, and one measures the outcome that eventually occurs.

I find that many misunderstandings about volatility investing come from mixing these concepts together. Once you separate them, the logic behind volatility markets becomes much easier to understand.

Takeaways

- Historical volatility measures how much prices moved in the past.

- Implied volatility reflects the market’s expectations about future uncertainty.

- Realized volatility measures what actually happens after those expectations are formed.

- No single volatility measure is sufficient on its own.

- Comparing implied and realized volatility helps investors understand volatility premium opportunities.

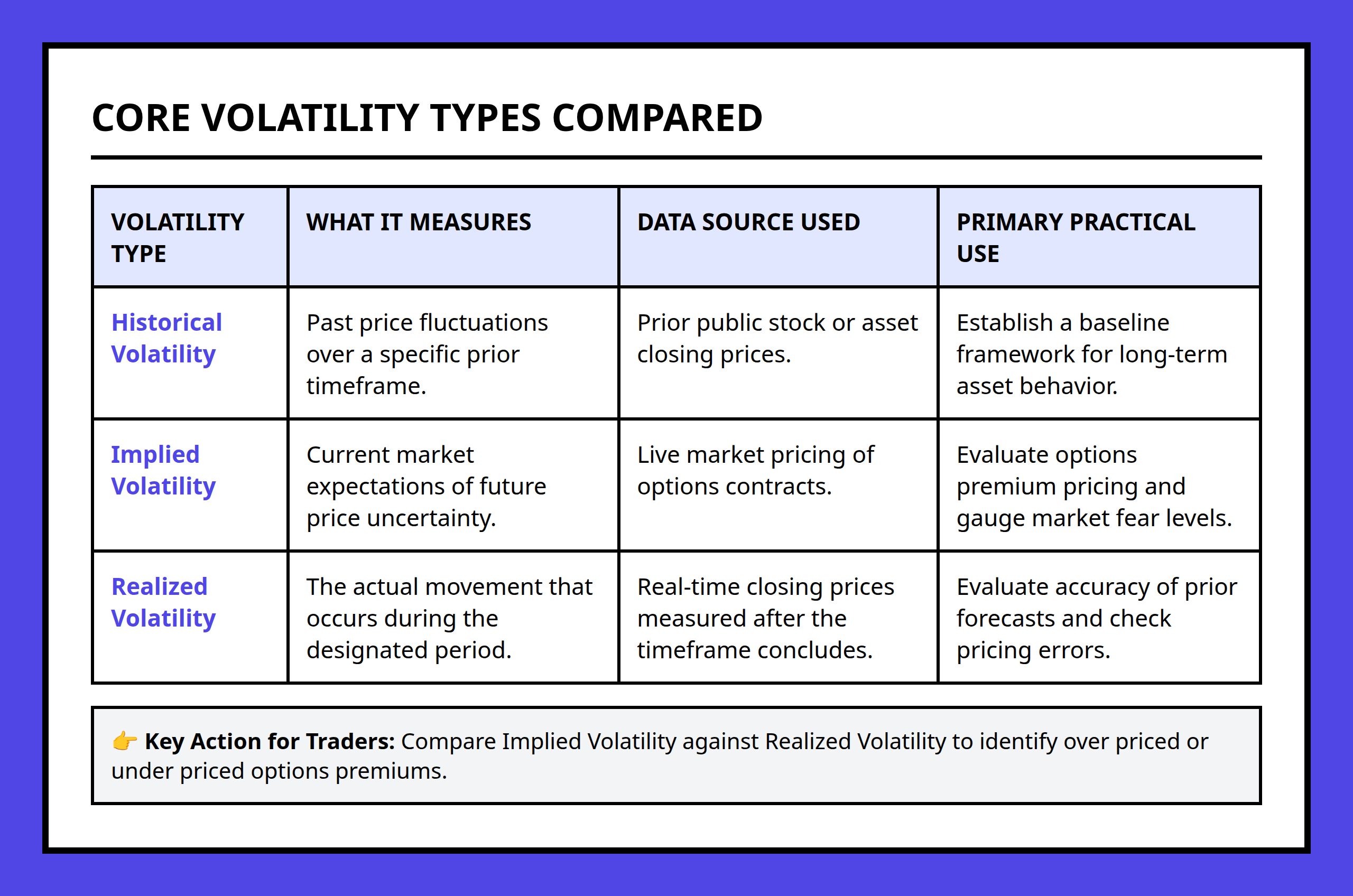

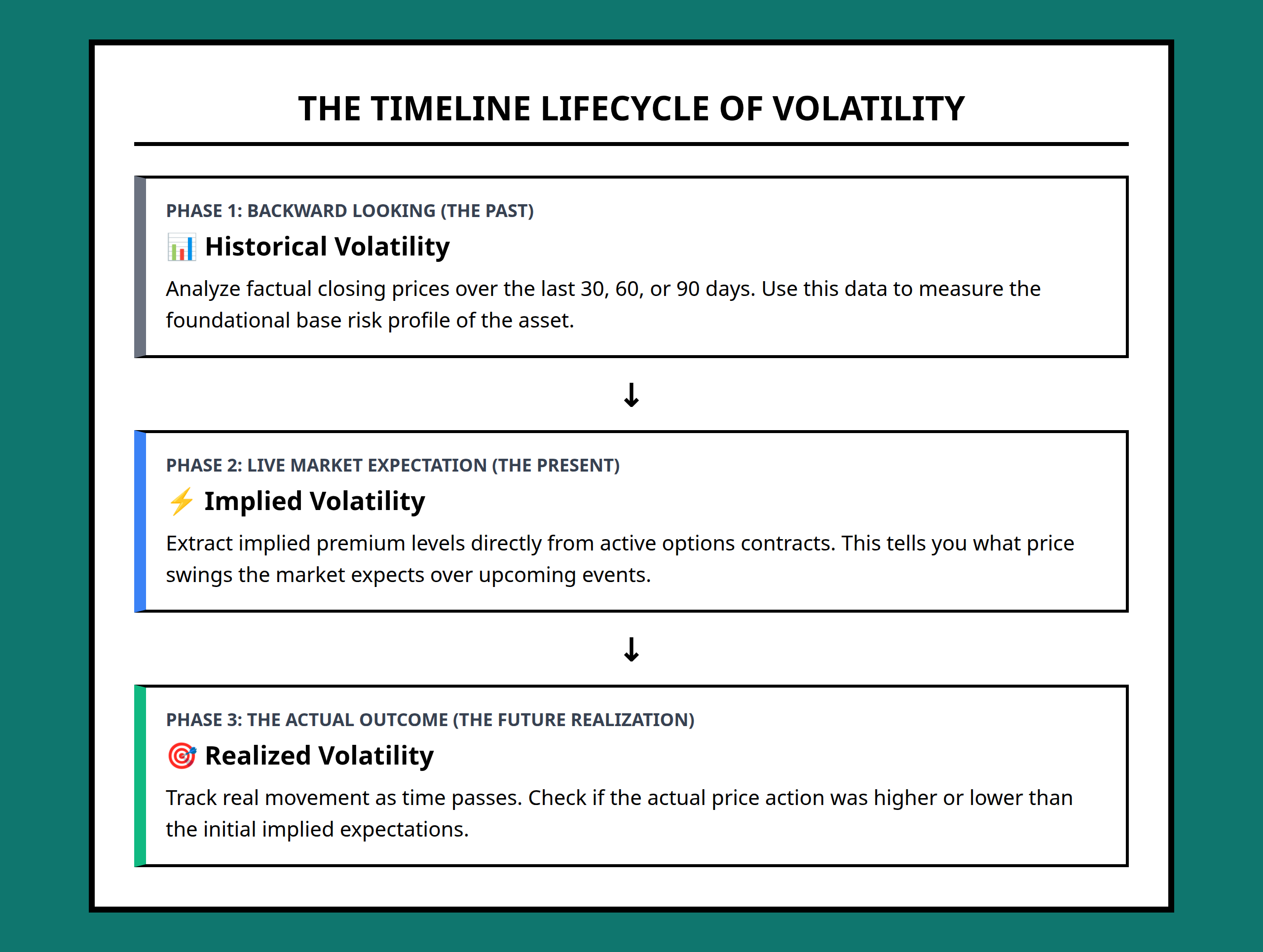

Historical Volatility: Looking Backward at Market Behavior

Historical volatility measures past price movement. It is calculated from previous market returns and provides a statistical picture of how much an asset has fluctuated over a specific period.

If an asset experienced large price swings over recent months, its historical volatility will be higher than an asset whose prices remained relatively stable.

The value of historical volatility is that it provides objective evidence of what has already occurred. Investors can use it to understand how turbulent or calm a market has been.

However, historical volatility has an important limitation: it only describes the past.

A market that was calm last month may become highly volatile next month. Historical volatility offers context, but it does not directly tell investors what will happen next.

That distinction becomes important when comparing it with implied volatility.

Implied Volatility: What the Market Expects

Implied volatility reflects expectations about future volatility. Rather than being calculated from past price movements, it is derived from option prices and represents the market’s collective view of future uncertainty.

When investors become concerned about potential market turbulence, demand for protection often increases. As demand rises, option prices can increase, causing implied volatility to rise as well.

Because of this, implied volatility often acts as a forward-looking measure of uncertainty.

It is important to remember that implied volatility is not a forecast guaranteed to be correct. It reflects what market participants expect, not what will necessarily happen.

| Volatility Type | Primary Focus | Time Perspective |

|---|---|---|

| Historical Volatility | Past price movements | Backward-looking |

| Implied Volatility | Expected future volatility | Forward-looking |

| Realized Volatility | Actual future outcome | Observed after the fact |

One way to think about implied volatility is as the market’s estimate of future weather. It reflects expectations based on available information, but actual conditions may turn out differently.

Realized Volatility: What Actually Happens

Realized volatility measures the volatility that ultimately occurs.

After a future period has passed, investors can calculate how much prices actually moved. This becomes realized volatility.

Realized volatility serves as the scorecard for volatility expectations.

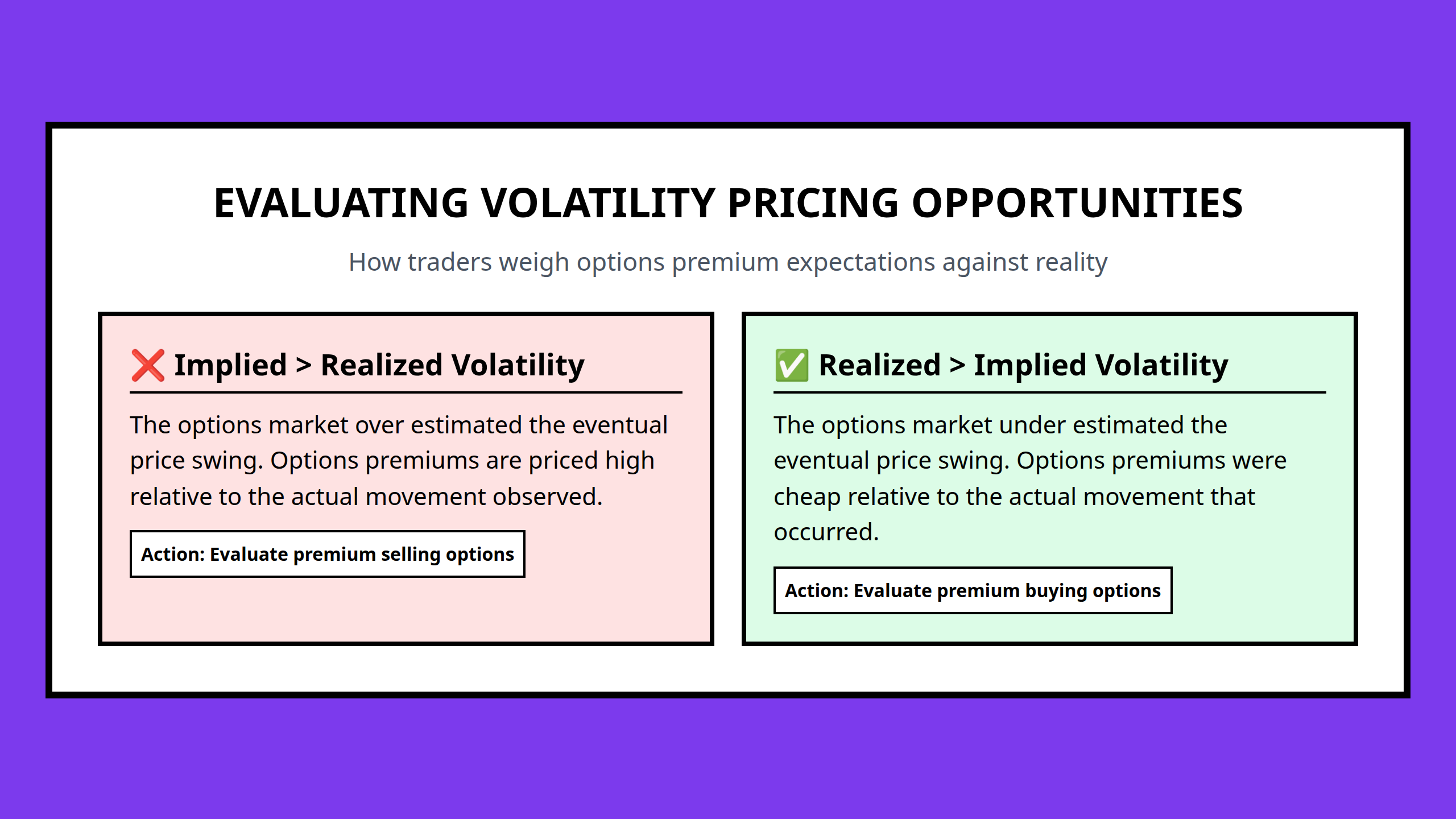

If implied volatility suggested that markets expected large price swings but actual movements were relatively modest, realized volatility would be lower than implied volatility. If markets experienced more turbulence than expected, realized volatility would be higher.

This comparison is central to many volatility-based investment strategies.

The difference between what investors expected and what actually occurred can create gains or losses depending on how volatility positions were structured.

Why the Difference Matters for Investors

The relationship between implied and realized volatility helps explain how volatility investing works.

Many volatility strategies depend on whether market expectations accurately reflect future outcomes. Investors are often willing to pay for protection against uncertainty, which can cause implied volatility to exceed realized volatility over long periods.

This difference helps create what is commonly known as volatility premium.

Understanding this relationship is important because it reveals that volatility investing is not simply about predicting market direction. Instead, it often revolves around evaluating expectations versus reality.

Consider an illustrative scenario. Suppose investors become highly concerned about future market risk and pay elevated prices for protection. If market conditions later turn out to be less dramatic than feared, realized volatility may end up lower than implied volatility.

The key insight is not whether markets went up or down. The key question is whether actual volatility matched expectations.

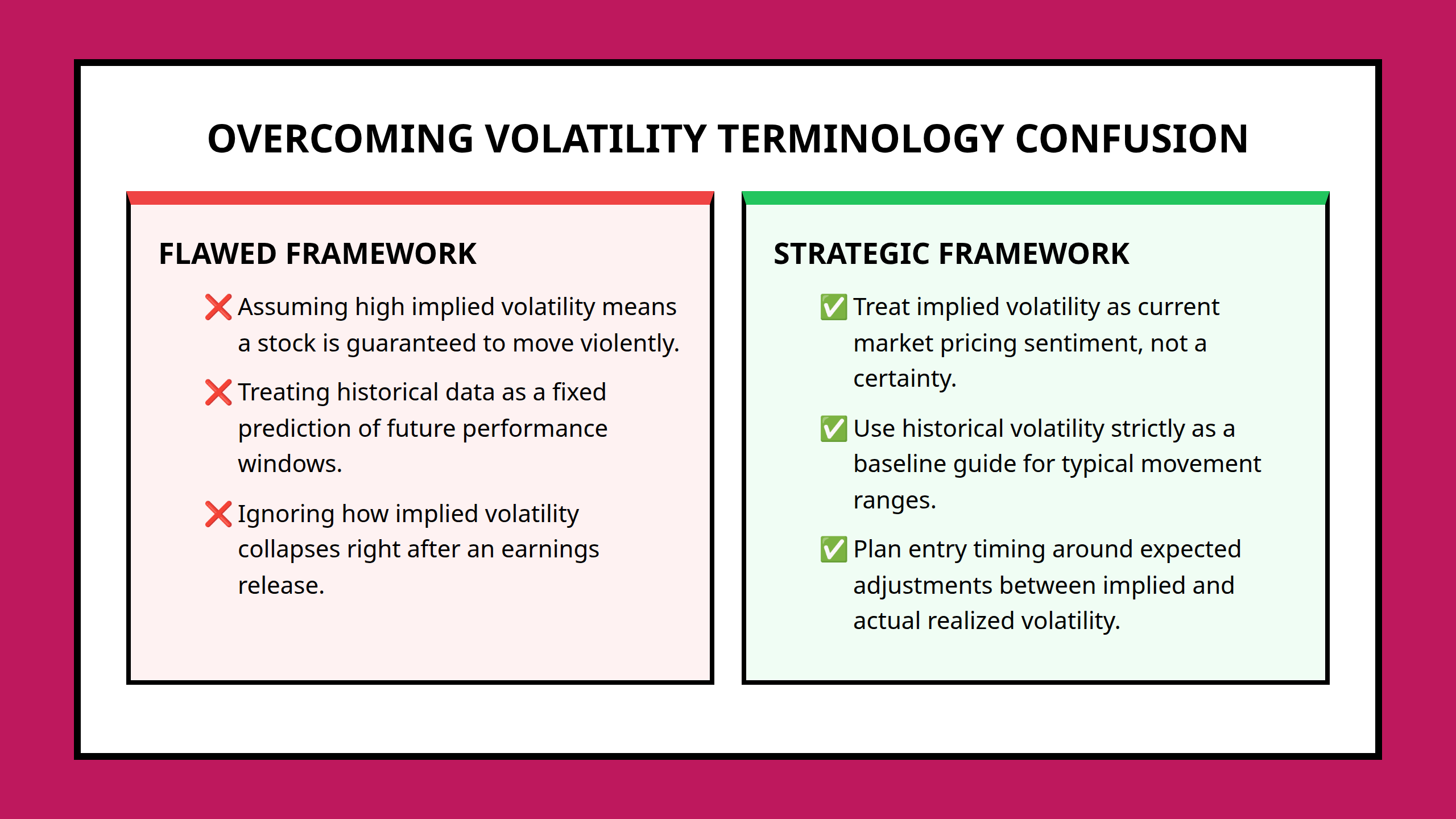

Common Mistakes When Using Volatility Measures

One common mistake is treating implied volatility as a perfect prediction. It is better viewed as a market expectation than a certainty.

Another mistake is relying entirely on historical volatility. Past behavior provides useful information, but markets can change quickly.

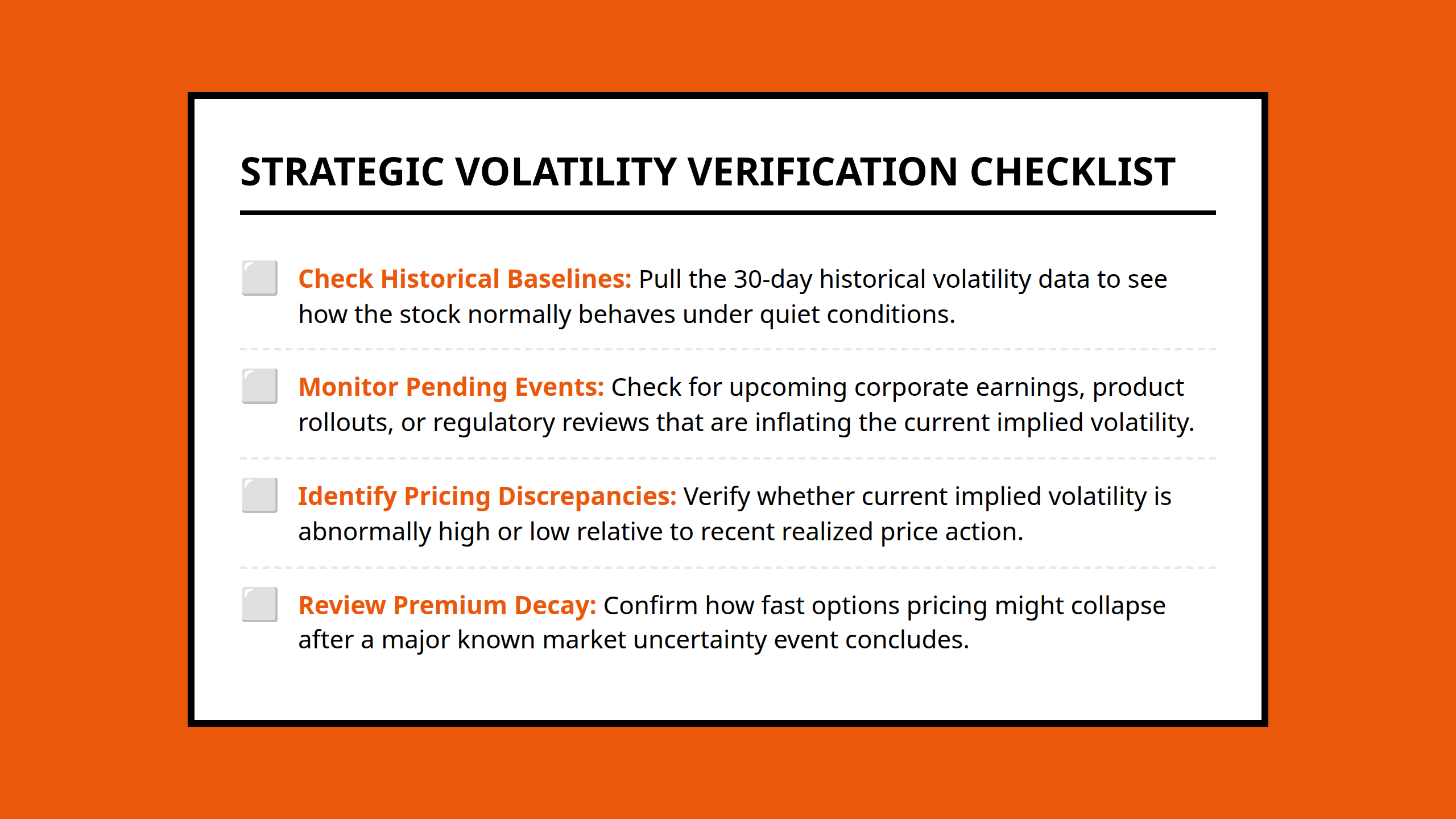

A third mistake is examining volatility measures in isolation. Each metric provides a different perspective, and their greatest value often comes from being analyzed together.

Investors who understand all three measures gain a more complete picture of market risk than investors who focus on only one.

When evaluating volatility, a practical habit is to ask three separate questions: What happened before? What does the market expect now? And what eventually occurred? Those questions naturally align with historical, implied, and realized volatility.

FAQ

- Historical Volatility: A measure of how much prices moved in the past based on historical returns.

- Implied Volatility: The market’s expectation of future volatility, derived from option prices.

- Realized Volatility: The actual volatility observed over a future period after it has occurred.

- Volatility Premium: The potential return associated with the gap between expected volatility and actual volatility.

- Options Market: A market where contracts are traded that allow investors to gain exposure to future price movements and uncertainty.

- Market Expectations: Collective beliefs reflected in asset prices about future market conditions.