Bond prices fluctuate as interest rates change, but duration and convexity provide practical tools to estimate and manage this risk, helping investors make informed portfolio decisions.

Interest-rate risk is a major concern for anyone holding bonds. I often remind myself that small changes in interest rates can have significant effects on bond prices, depending on their maturity and coupon structure. Understanding duration and convexity allows me to quantify that sensitivity and take more informed actions. It shifts the focus from guesswork to structured risk management.

Rather than only looking at individual bond yields, I consider the portfolio’s overall exposure to interest rate changes. Duration and convexity give me a framework to compare bonds with different characteristics and to estimate potential price movements under different interest rate scenarios.

Takeaways

- Duration measures a bond’s price sensitivity to interest rate changes and is a foundational tool for estimating interest rate risk.

- Convexity accounts for the curvature in the price-yield relationship, improving the accuracy of price change estimates.

- Combining duration and convexity allows more precise risk management than relying on duration alone.

- Investors can use these measures to immunize portfolios or strategically position them based on interest rate forecasts.

Understanding Duration

Duration is a weighted average of the time until a bond’s cash flows are received. It approximates how much a bond’s price will change for a 1% change in interest rates. For example, a bond with a duration of 5 years would decline roughly 5% in price if rates rose by 1%. Duration also helps compare bonds with different maturities and coupon rates in terms of their interest rate sensitivity.

The Role of Convexity

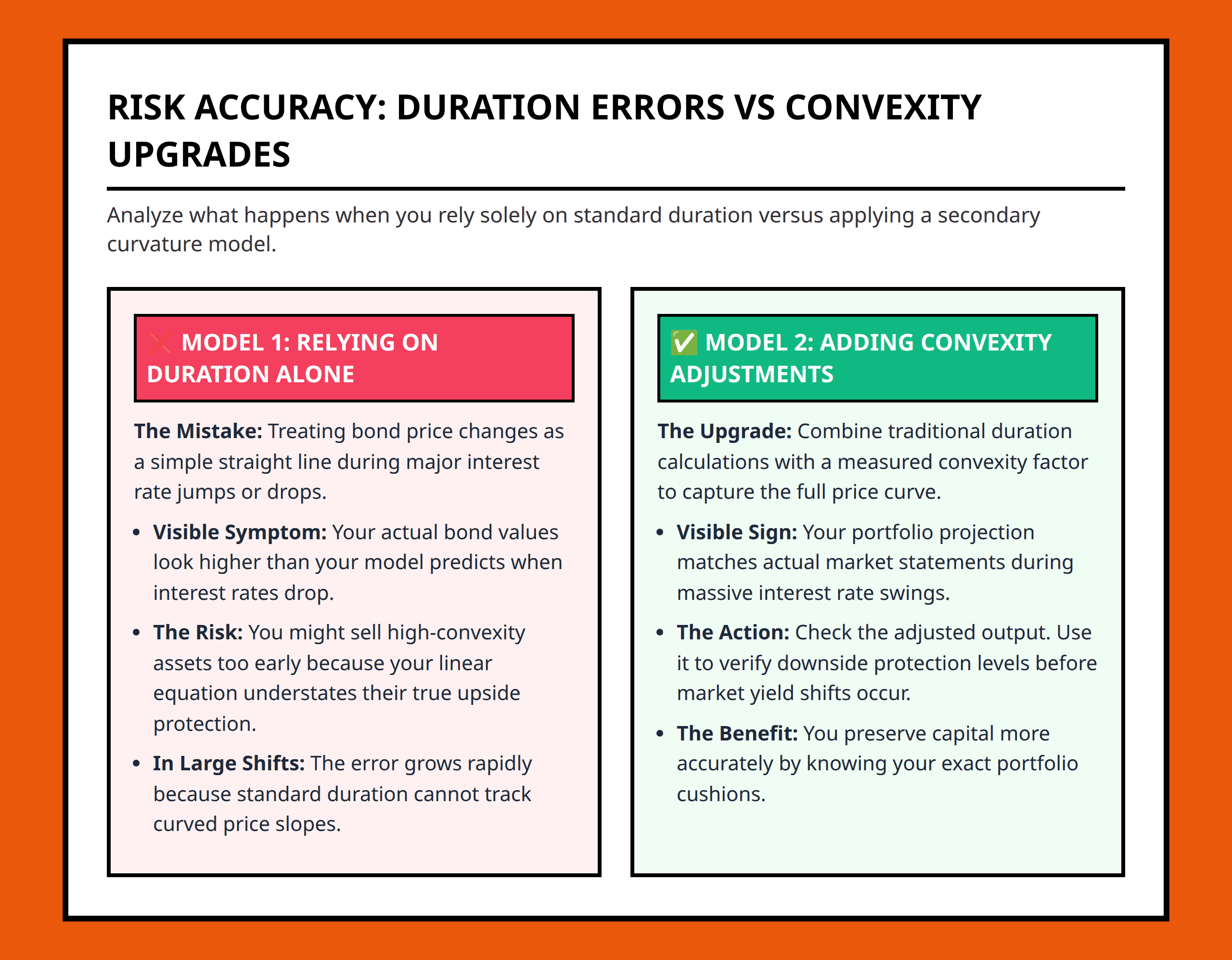

While duration provides a linear estimate of price change, the actual relationship between bond prices and yields is curved. Convexity measures this curvature and refines the price change estimate, especially for larger rate movements. I find it crucial for bonds with longer maturities or lower coupons, where duration alone might underestimate or overestimate price changes. Convexity ensures my risk estimates remain realistic under varying rate conditions.

Limitations of Duration Alone

Using duration without considering convexity can be misleading, particularly for bonds with long maturities or when interest rate shifts are large. Duration assumes a straight-line relationship, which over-simplifies reality. By including convexity, I can better anticipate non-linear price movements and reduce the chance of unexpected losses in volatile interest rate environments.

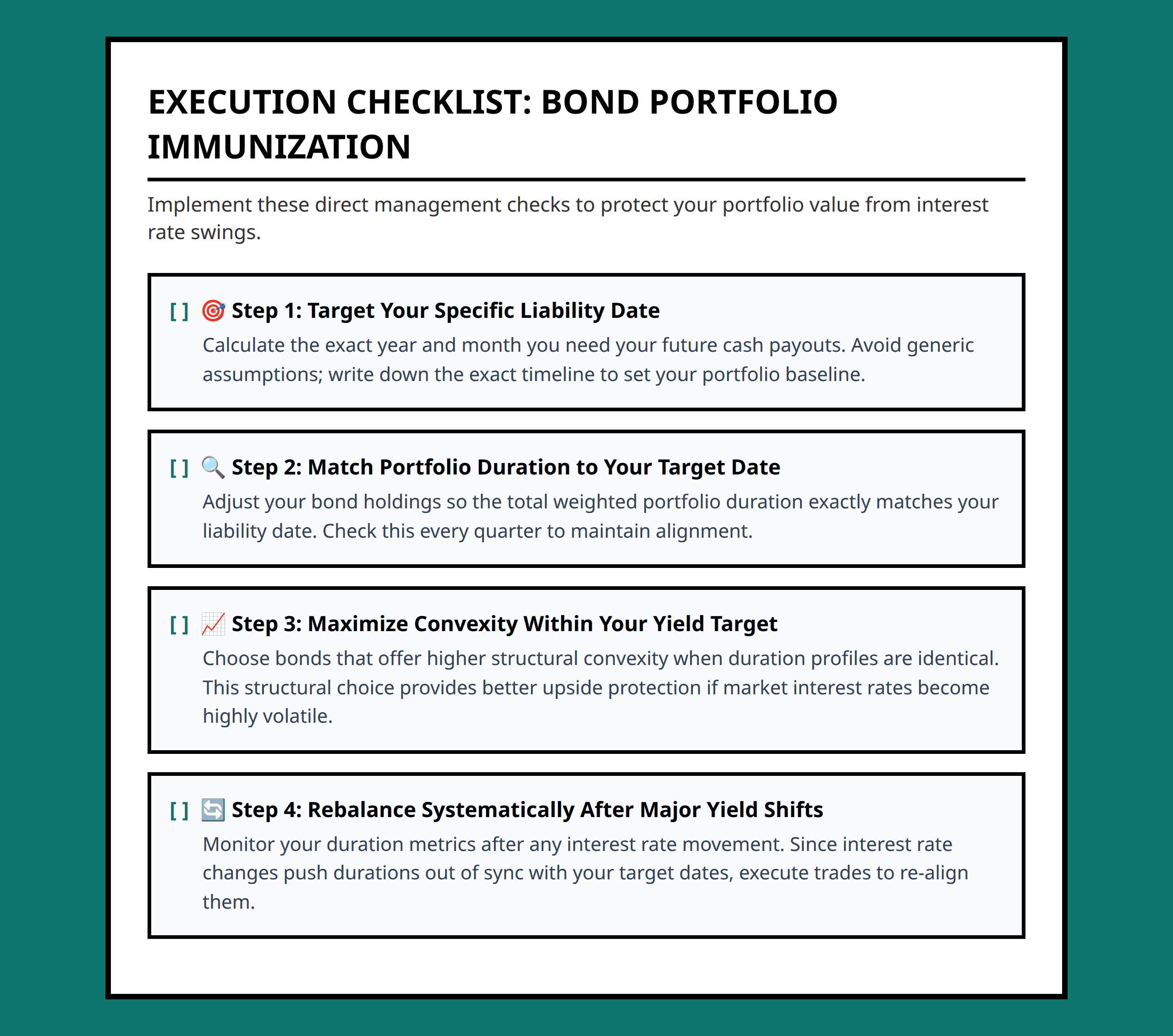

Applying Duration and Convexity to Portfolio Management

Once I understand a bond or a portfolio’s duration and convexity, I can make strategic choices. For example, I may immunize a portfolio to protect against rate changes or adjust exposures based on my interest rate outlook. Active management using these tools allows me to structure my portfolio for a targeted risk profile, balancing income goals with sensitivity to interest rate movements. This approach helps avoid surprises and supports more consistent long-term returns.

- Duration: A measure of a bond’s sensitivity to interest rate changes, representing the weighted average time until cash flows are received.

- Convexity: A measure of the curvature in the price-yield relationship of a bond, refining the estimate of price changes.

- Interest-Rate Risk: The potential for bond prices to decline due to rising interest rates.

- Immunization: A strategy to structure a bond portfolio to offset interest rate risk.

- Active Bond Management: Adjusting bond holdings to optimize returns and manage risks based on market conditions.

References:

- https://www.raymondjames.com/wealth-management/advice-products-and-services/investment-solutions/fixed-income/bond-basics/duration-and-convexity

- https://www.investopedia.com/articles/bonds/08/duration-convexity.asp

- https://madisoninvestments.com/interest-rate-risk-understanding-duration-convexity/

- https://www.linkedin.com/top-content/finance/fixed-income-securities/bond-duration-and-convexity/

- https://www.fidelity.com/learning-center/investment-products/fixed-income-bonds/duration

- https://globalmarkets.cib.bnpparibas/convexity-hidden-risk-in-low-rate-world/

- https://www.researchgate.net/publication/364568523_Research_on_Interest_Rate_Risk_Management_Based_on_Duration_Convexity_and_Immunization

- https://www.poems.com.sg/glossary/bonds/convexity/

- https://www.linkedin.com/posts/affanmohsin_bondmarkets-fixedincome-riskmanagement-activity-7379195914822946817-kwjz

- https://www.reddit.com/r/bonds/comments/1no2mmw/how_do_you_use_duration_and_convexity_to_predict/

- https://www.reddit.com/r/CFA/comments/awxpy1/why_are_duration_and_convexity_are_higher_for_a/

- https://www.investopedia.com/terms/d/duration.asp

- https://www.reddit.com/r/bonds/comments/1no2mmw/how_do_you_use_duration_and_convexity_to_predict/nfoyc8r/

- https://www.reddit.com/r/bonds/comments/1no2mmw/comment/nfqyvlp/